Your cart is empty.

Keep shopping

Teach on Udemy

Turn what you know into an opportunity and reach millions around the world.

Learn MoreValuable Stock Market Investing Strategies for Beginners

Rating: 4.2 out of 54.2(180 ratings)

24,210 students

Valuable Stock Market Investing Strategies for Beginners

Discover effective investment strategies and the best stocks to buy right now.

Created byMatt Bernstein, Skillhance, LLC

Last updated 11/2018

English

What you'll learn

- Have complete understanding and confidence when investing in the stock market.

- Apply key stock investing strategies such as investing in Dividend Paying Stocks, Growth Stocks, Value Stocks, Stocks that have future Growth At A Reasonable Price (GARP) and more.

- Apply best practices and techniques to make better stock choices.

- Determine whether an Online Discount Broker, Full-Service Broker, Financial Planner, Robo-Financial Planner or other service to place stock orders is right for them.

Explore related topics

Course content

4 sections • 21 lectures • 1h 42m total length

- Introduction to Investing2:37

Developing an Investor's Mindset

Ask yourself this question; why are you watching this video innovation series and what are you hoping to get out of it?

The most common reason is because you have a desire to make and grow your money. I must caution that it is rare for someone to make a living just by trading in the stock market; rather the markets are a tool that provides the opportunity for turning the money you have already earned at your day-job into earning even more money.

Fear is another common motivator for watching this video innovation series. Everyone has heard of the stock market and the stories of how it can make or break your bank account. It is normal to fear the potential losses but all the while desire the lucrative gains. I’m here to ease your market anxiety.

Others might have tried their hand at investing but found little to no success. With this course I offer up to you the chance to view the markets from my own perspective and what I have found to be successful.

Hi, my name is Matt Bernstein from Low Cost Hustle and there are three main ideas you’re going to learn throughout the course of watching.

First, an introduction to the market. Whether you’re completely unfamiliar with market terminology or not, there is a lot of material to cover here. If you’re confident in your understanding of the market concepts and terminology, you may skip to the second section on thinking rationally. But keep in mind that you had to learn all the letters of the alphabet before you write full sentences.

Second, I’d like to help you get the proper mindset that is necessary for success in the stock market, and that is overcoming your emotions to think in a rational way. I can’t even begin to tell you how many stories there are of people who let their emotions get the best of them and lost out for it. We’ll go through real-life scenarios that will steer you in the direction of a favorable mindset and also provide some history on the markets.

Third, I’d like to take you through the process of how I research stocks for my own portfolio, as well as how I maintain a portfolio to meet my own personal goals. I will explain how I have earned double-digit returns year in and year out.

With this video course, I intend to impart the knowledge and way of thinking that I have developed over the years. I promise that by the end of this series you will walk away with the tools and know-how necessary to outperform well-known benchmarks like the DOW and S&P 500.

So with that, I invite you to learn everything I know about the market and what it takes to outperform it.

- What is the Stock Market?6:09

The Stock Market

You’re watching this video series with the intention of learning a lot about the stock market, how to make money from it and so on. Well what is the stock market? The stock market in its current form is an electronic exchange where investors can buy or sell shares of stock in a company; kind of like a giant marketplace where the only thing for sale are shares of stock. When you buy a share in a company you are actually buying a piece of the company. So now that you own a share, you are counting on the company to make lots of money so that your shares of stock increase in value. Similarly, if the company makes no money or even loses money, the value of your share will decrease. And so the stock market consists of a great deal of investors who are looking to buy shares of companies that will perform well into the future, and sell the shares of companies that will perform poorly. If you happen to be good at forecasting the future, you can make a great deal of money in the stock market. In section three I will talk about some of the common strategies that myself and others use to try to predict which stocks will go up and down.

Its important to have a firm understanding of what determines the share price of stock. We’ll get into ways of calculating value in section 3 but for now all you need to know is that the market determines the share price. That is, the price is determined by what investors are WILLING to pay for a particular share. As of this writing a single share of Google (GOOG) is valued at over $1,100 whereas a single share of Microsoft (MSFT) is hovering around $36. I want to be clear that these prices DO NOT say anything about the value of the company itself, rather these prices are merely a function of what the investors in the market are willing to pay. And so the fact that shares of Google (GOOG) are trading over $1,100 means that collectively, investors in the market think that one share of Google (GOOG) is worth over $1,100. Human emotion and psychology play a significant role in the pricing of stocks. This is a very important concept that I’d like you to always remember because people can and do have poor judgment from time to time and end up paying too much or too little for any particular stock. Note: There is a lot of money to be made if you can figure out when a stock is over or underpriced.

In addition to stocks, there are other financial instruments I’d like to mention here. I won’t go into great detail in this series because I personally only trade stocks. But I think its important to be aware of what else is out there. I’m sure you’ve all heard of bonds before and possibly options, derivatives and money market instruments.

Bonds are fundamentally different from stocks in that they are a debt instrument. Whereas stock is equity. In the most general sense, debt, in this case a bond, guarantees the bond owner a claim on the value of that bond. For example, if you own a bond with a face value of $1000, you would expect to be paid back $1000 by the company that issued the bond. On the other hand, owning equity, in this case common stock, does not entitle the owner to anything. In other words, purchasing a share of Google (GOOG) for $1000 does not mean the company owes you $1000. It’s a strange concept to understand but ties hand-in-hand with what I was speaking of earlier. That is, the value of stock lies only in what other people are willing to pay for it. Now you might be wondering why anyone would ever buy stock if they weren’t guaranteed the amount they paid for it. Well the answer lies in the methods that people have developed for valuing the worth of a stock; a topic we will discuss later.

Options and derivatives can be confusing to talk about at first so I won’t dive in here. All you have to know for now is they are complicated ways of trading the stock markets that don’t require an investor to actually purchase stock in the common sense of the word. If you are new to the markets, do not; I repeat do not try to trade options. You can end up losing a lot of money if you don’t know what you are doing.

There are two terms you should be familiar with to understand money markets and those are liquidity and maturity. In finance, the liquidity of something represents how quickly and easily it can be converted into cash, with the basic assumption that cash itself is the most liquid asset of all and that a $1 dollar bill can always be traded for another $1 dollar bill. Whereas a house for example is not very liquid because it can take a great deal of time to sell for cash and the price is usually negotiable; that is a house valued at $500,000 might actually be sold for $480,000.

When we talk about the maturity of something in finance we are referring to the length of time the instrument is outstanding. The U.S. government regularly issues Treasury Bills, commonly referred to as T-Bills with varying maturities ranging from 1 month to 6 months. As a new investor the only two money market instruments you need concern yourself with now are T-Bills and Certificates of Deposit. Certificates of Deposit, or CDs are generally issued by a bank and have varying maturities. The basic premise is you hand over $1000 today, and the bank agrees to give you you’re $1000 back plus interest at the end of maturity.

Lets quickly recap what you’ve just learned:

The stock market is an electronic exchange that allows you to trade shares of a company with other investors. By “buying low and selling high” as they say it is possible to profit off these transactions.

The price a stock is bought or sold for is constantly changing second by second and is determined by how much money an investor is willing to pay to own a share. This is the idea of supply and demand.

There are a number of other tradable financial instruments such as bonds, options, and derivatives, that are good to be aware of but we won’t discuss frequently in this course.

Money market instruments are very liquid, that is they can easily be traded for cash, and have short maturities. The two to be familiar with for now are T-Bills and CD’s.

- Learn Stock Market History4:42

Historical Market Returns: What to Expect

Hi, Matt Bernstein here to talk about the historical performance of the market. There are numerous sites out there offering free historical price data on the markets, and if you’re willing to pay there are some that offer even more in-depth data. I like to use Yahoo! Finance because it is free, simple to use, and meets most of my needs. There is also the convenient option to download any set of data right onto a spreadsheet for you to do with what you like.

When measuring the performance of the stocks we own it’s useful to have a benchmark to compare with so we know how well we are doing. From 1926 to 2009 the average rate of inflation was about 3%. This means that each and every year, the cost of goods rose by about 3%. And so if you pay $10 for a watermelon today, you can expect an identical watermelon to cost $10.30 a year from now. And in 10 years that same watermelon now costs $13.44. What this really tells us is that the money under our mattress loses value over time. And so to keep our money from degrading in value, it’s a good idea to invest it in things that grow faster than the inflation rate of 3%.

Money markets typically have the lowest earnings potential of the investment classes with a historical return rate of about 3.7%. If you invested your $10 in money market instruments, then in 10 years you could expect to now have $14.38. Enough to buy a $13.44 watermelon and have some change left over. As you can see, we have successfully beaten the rate of inflation but only barely.

Bonds fared a little better over the same time period (1926 – 2009), averaging a return rate of 5.5%. The same $10 investment in bonds will be worth $17.08 in 10 years. We made some money but as you can guess there are better alternatives out there.

If you wish to grow your money faster than this, you must find other investment avenues. The truly great thing about the stock market is that it offers the opportunity for much quicker growth than either bonds or money markets.

Large-Cap stocks, those that represent the largest companies in the world, (i.e. the Coca-Cola’s, Exxon Mobil’s, & Microsoft’s of the world) have a 9.8% return rate over the same time period (1926 – 2009). And after 10 years our $10 dollars is now worth $25.48.

Small-Cap stocks, those that represent comparatively smaller companies, have an even more impressive 11.9% return rate over the same time period. In just 10 years our $10 has more than tripled to $30.78. You can now buy 2 watermelons for $13.44 and still have money left over.

It gets better: the large-cap and small-cap average rates of returns are calculated using every stock that meets those size qualifications over that time period. And so these averages also include the stocks of companies that floundered or even went bankrupt. So think of it this way: if you picked 100 small-cap stocks completely at random – meaning some will do great, some will do okay, and some will go bankrupt, you could expect to receive an average return rate of 11.9%. Which means if you had a knack for picking small-cap stocks that didn’t go bankrupt, you could expect a higher than 12% return rate. So when we talk about beating the market we literally mean achieving a higher rate of return than the market averages on its own.

For comparison, my brokerage account lists my average rate of return at a little over 44% each year since its inception. Over that same time period (a little over 5 years) the S&P 500 has averaged returns of just over 17%. And so you can see that I was able to earn 27% more than the market over this 5-year period. In finance, the returns we generate above and beyond the benchmark are known as Alpha, meaning I was able to generate +27% alpha.

Set a goal for yourself: and that is to strive to beat the average market return of 12% each and every year, because otherwise, you might as well just pick stocks at random.

- Should You Use Financial Advisors?6:01

How Good Are Financial Advisors?

Last video we talked about the average performance of different categories of investments, and we learned that an investor that picks stocks at random could expect average gains of about 12% each year. Which must mean that if we are selective in what stocks we purchase, we could expect greater than 12% returns.

Hi, Matt Bernstein from Low Cost Hustle and this video will give you an idea of how well professional money managers do.

Lets begin by looking at the performance of mutual funds. For those of you unfamiliar with the term, mutual funds allow a large group of investors to pool their money together to buy any number of stocks. Run by one or more money managers, mutual funds provide investors with access to a professionally managed portfolio of stocks. They aren’t free and some of them have very high expenses and fees. Investors invest in mutual funds with the belief that the money manager knows how to generate high returns – it is after all their job. Surprisingly, studies show more often than not that mutual funds fail to beat the performance of the broader market. Although professional money managers often have advanced degrees in Economics and Finance from some of the best business schools, studies consistently show that only 1 in 4 mutual funds outperform the market. This is a shocking result that shows three-quarters of funds performing worse than an individual picking stocks at random.

But the truth is more complicated. Just like you and me, professional money managers want to make as much money as possible, and often that comes at the expense (literally) of their investors. It turns out that high fees and expenses are one of the main reasons for this trend of underperformance. Although many of these fund managers are quite good at stock picking, the fees and expenses they charge can end up eating a large chunk of the gains passed onto the investor. And so a fund that earns a 14% return on its investments but charges 3% in expenses actually ends up underperforming the market average of 12%.

Does this mean we should avoid mutual funds? Well that depends on a number of factors including and not limited to:

how old you are

how much money you have to invest

Do you have enough time to do research on your own?

I would argue that if you aren’t:

elderly or already retired

don’t have more than $10 million dollars

or aren’t too busy during the day to research stocks on your own.

Then the benefits of investing on your own versus in mutual funds outweigh the negatives.

Before we go further I’d like to explain two terms you should be familiar with: and those are “sectors” and “indices”. When we talk about indices the Dow Jones, NASDAQ, and S&P 500 are the most frequently mentioned. And the purpose of these indices is to track the performance of a group of stocks. So for instance, the S&P 500 tracks the performance of the 500 largest companies in the United States. When we say that the S&P 500 is up by 10 points today, we mean that the average increase in stock price of all 500 of those stocks was 10 dollars. Some of those stocks will have risen higher, some lower, and some will have even lost value, but on average the index was up 10 points. The Dow Jones, also known as the Dow 30, the Dow Jones Industrial Average, or simply the Dow, is an index that tracks 30 very large companies in the United States. And the NASDAQ Composite is an index that tracks the performance of about 3000 stocks, most of which are technology companies. There are many more indices but these three are the most commonly mentioned.

Sectors describe a particular sub-group of the economy. Technology, Finance, Energy, and Utilities are examples of different sectors and they all have very different behaviors due to the different markets they represent. It is common, for example, to use the NASDAQ Composite as a gauge for how well the Technology sector is doing, and the Dow and S&P 500 are gauges for the overall economy.

In recent years Exchange Traded Funds known simply as ETF’s have been gaining in popularity. ETF’s are like mutual funds in that they hold any number of stocks. However, unlike mutual funds, a money manager does not choose the stocks an ETF holds. Rather an ETF is typically used to mimic as closely as possible a particular index or sector. For example, if you wanted to match the performance of the S&P 500, then rather buying into all 500 stocks one-by-one, you could by an S&P 500 ETF, the most famous of which is the Spider SPY. Whereas if you wanted to match the performance of financial companies only, you might invest in a financial ETF, the most popular being the Spider XLF. The advantage of ETF’s is that they allow investors to trade entire indices and sectors as if they were single stocks.

ETF’s do have fees and expenses but they are usually lower than those of mutual funds. And it turns out that for the same reasons as with mutual funds, the average ETF fails to beat the market because of said fees and expenses. Does this mean you should avoid ETFs? For the passive investor without time to do research on his or her own, I would argue ETF’s are a better option than mutual funds, due largely to the smaller fees and expenses. But for the active investor looking to beat the market, individual stock selection is the way to go. If someone else is doing the heavy lifting for you, then you can be sure they are taking a cut for themselves.

So I hope this video has given you an idea of the advantages of investing on your own versus entrusting your money to someone else. If you’re willing to take some time to do your own research then it is very possible to achieve a much higher return than what most money managers can offer.

- Start Planning for Retirement5:35

Retirement

Hi, Matt Bernstein from Low Cost Hustle here to talk about the benefits of retirement accounts. In addition to a discussion on 401k’s I will also explain the differences between a traditional and a Roth IRA.

Gone is the day when we can rely on social security and pensions to take care of all our retirement needs. It is now necessary for Americans to fund at least a portion of their retirement on their own. Most employers now offer 401k plans instead of a pension. If your employer has a 401k plan I recommend you sign up immediately if you have not already. Once signed up for a 401k plan, your employer will automatically deduct a percent of your salary to be placed in your 401k funds. Your 401k is just an account that invests your salary deductions into the stock market with the idea being that over time this will add up to a lot of money. And what’s better is most employers will match your contribution up to a certain limit. So if you are contributing say 6% of each paycheck to your 401k, your employer will kick-in an additional 6%. Yes, your employer is literally paying you extra money towards your retirement fund out of their pocket. Many 401k plans do not allow you to pick and choose individual stocks, but instead provide access to mutual funds and ETFs. If this is the case, look for an option that offers “high-growth” or “high-risk”. Some funds will have “technology” or “biotechnology” in the name: as a rule of thumb these tend to be high-growth and high-risk funds. If your employer offers a 401k plan, sign up TODAY and opt for the max-allowed contribution.

In addition to 401k’s there is another type of retirement account known as an IRA. An IRA is just an account you contribute money to with the intention of saving it for later. Unlike many 401k plans, you may invest your IRA contributions into single stocks, bonds, CD’s, and really anything else with the exception of options and derivatives. The most frequently mentioned are the Traditional and ROTH IRA’s.

The traditional IRA is the more common of the two and anyone under the age of 70 and a half may open one and contribute. Currently, if you are younger than 50 years of age, you are allowed to contribute $5,500 to your traditional IRA each year. And those over 50 may contribute $6,500. A traditional IRA is a tax-deferred investment vehicle, meaning - only once you begin withdrawing the money in your retirement are you taxed on it.

Similarly the Roth IRA also allows contributions of $5,500 for those under 50 and $6,500 for those 50 or older. However, you are only allowed to make the full contribution if your yearly income is less than $114,000 – there’s a reason for this and it has to do with giving a tax-break to Americans that aren’t considered “rich”. With a Roth IRA you pay your taxes before you contribute the money after which it grows tax-free. So no matter how large the amount in your Roth IRA grows too, you pay no taxes on it when you begin withdrawing money in retirement. I personally have a Roth IRA and make the maximum contribution each year. I recommend the Roth over the traditional if meet the income requirement. Those that contribute the max-allowed to both their 401k and IRA will find themselves living very comfortably come retirement.

Lets do a quick overview of some possible scenarios to see just how much money you can hope to have:

We will assume that you can earn the historical market rate of return of 11.9% on your investments, that your employer will match 401k contributions up to 6% of your salary, that your salary is $50,000, and that you retire at age 55.

For the first scenario I have given an example of someone that does not participate in their company’s 401k plan and saves $5,500 each year but chooses to not invest it in the market. Perhaps they simply keep it in a savings account or under their mattress. As you can see, an individual that invest their money in the stock market has a much more comfortable retirement than someone who does not. And also the earlier you begin contributions to your retirement account, the better off you will be. Someone famous once said that the power of compounded returns is the most powerful force in the world. And here we can see how big a difference just 5 years can make. The person that started at age 20 earns over $2 million more than the person that begins at age 25.

As an added note, these scenarios don’t take into consideration any raises in salary or a better than 11.9% rate of return. These numbers begin to grow much bigger if you take these things into account.

Please realize that it is never too late to start saving for retirement but the earlier you start the better off you will be.

It is much more advantageous to first max out your IRA and 401k contributions but for those that want to earn even more money in the markets, there is also the option of opening up a brokerage account. A brokerage account allows you almost unlimited freedom in your investment decisions, both in the amount you can invest and what you can choose to invest in.

I hope that you at least take advantage of the IRA option but also the 401k options if your company offers them. It really is an opportunity to turn your money into more money, but only if you make sensible decisions. In the coming videos I will explain to the best of my ability how to take luck out of the equation so that you can reach the goals that you want.

- Old School Investment Strategies2:24

- Signing up for a Brokerage Account1:28

- Think Rationally About Investing6:21

Thinking Rationally

What does it mean to think rationally? A Google search reveals the definition of the word rational as “based on or in accordance with reason or logic”. And so it follows that to think rationally, one must make logical and reasoned deductions. Stated in another way, thinking rationally requires the absence of emotional bias.

Humans are emotional creatures and for a good reason: our emotions have helped our species survive as long as we have. But there are many facets of life in which emotions can lead us down the wrong path. It happens that the stock market is one such place where emotion is best left out of the equation.

You’ve probably heard of the saying “buy low and sell high” when it comes to investing. And at first glance it seems like an obvious piece of advice. But time and time again novice investors do the exact opposite.

Observe the most recent financial disaster:

In July of 2007, the S&P 500 reached an all-time high. In the months leading up to this, the market had been continuously climbing higher and higher. It just so happens that in the months leading up to this all time high, retail investors, that is mom and pop investors like you and me, began piling into the markets in droves. Having missed the last few years of amazing gains, the retail investors finally decided they would get in on the market.

But as fate would have it, in the months following the S&P’s all time high, the market began to crash. The United States faced one of the worst recessions since the 1920’s and the retail investors who had just decided to get in on the market were the worst ones hit. Institutional investors had known that a housing crisis was brewing and that the markets gains were unsustainable. In the months leading up to the S&P’s all time high, institutional investors began pulling funds from the market just as retail investors began investing.

So what happened? Well essentially, institutional investors, whom had been in the market for quite some time already, were selling their investments to collect their gains. That is they had bought low and sold high just as a rational thought process would dictate.

Retail investors on the other hand, had done the exact opposite; they got into the market near the highs, and then sold after it crashed, near the lows. They invested in the market near its highs because they had feelings of hopefulness and exuberance. Investing based on feelings turned out to be a huge mistake. Then once the stocks had continually hit lower lows, they pulled out their money - scared that they might lose everything they had invested. This was again a huge mistake as it was one of the greatest buying opportunities in recent history.

There is quote by Warren Buffett, perhaps the most successful investor of all time, that I want you all to memorize: “Be fearful when others are greedy and greedy when others are fearful.” What Warren is really telling us is to go against the herd mentality.

If you can recognize when stocks are significantly overvalued, it’s a sign that others are greedy. Have your exit plan ready.

If you can recognize when stocks are significantly undervalued, it’s a sign that others are fearful. You should begin buying hand over fist.

In late 2008 into early 2009, stocks had become incredibly discounted. There has perhaps never been a better time to find bargains in recent memory. The key was simply to recognize what the bargains were. In 2008 and 2009, there were bargains in all sectors, but the financials were particularly low-priced.

There were fear mongers shouting that the banks were going bankrupt and that the end of economic prosperity was over as we know it. This simply wasn’t true. At the time, the United States government could not afford to let the banks go under, and they showed that they would stand behind the banks no matter what. They literally gave hundreds of billions of dollars in bailouts. To me, this was an obvious signal to buy bank stocks. And so I began to research them heavily in an attempt to find the ones that were most undervalued. I purchased Bank of America stock and never once regretted it.

Always keep in mind that a market crash is an opportunity for you to buy stocks at prices you won’t see for years, perhaps even decades. Be sure you are positioned to capitalize on the opportunity when it knocks on your door.

Investors have searched for patterns in the market for as long as they’ve existed. And a few years ago I stumbled across a chart that found a negative correlation between the performance of markets and the sentiment of news headlines. It showed that as the headlines became more positive, the chance of a market crash in following months significantly increased, and that as the headlines became more negative, the chances of the market doing well in following months significantly increased. For example: it was more likely to see headlines of magazines and newspapers encouraging people to spend money on luxuries or to invest in the markets when they were near their peak. Conversely, headlines were more likely to warn of the dangers of investing after a market crash. Historically, headlines have told us to buy when we should be selling, and sell when we should be buying.

This turned out to be the most consistent indicator of any I have seen. And what it really provided me with was an insight into market behavior and psychology. It was like seeing the famous words of Warren Buffett “Be fearful when others are greedy and greedy when others are fearful” expressed in a graphical representation of data.

What’s more important is it provides a means with which to predict future market behavior. So remember: when everyone is yelling “buy, buy, buy” – it’s likely a sign of irrational excitement. And when everyone is yelling “sell, sell, sell” – it’s likely a sign of irrational fear.

- How the Housing Market Crashed4:17

Housing Bubble and the Crisis that Followed

I’d like to give a brief overview of the housing crisis that led to the recent market crash and one of the worst recessions the country has seen. The housing bubble, and the crash that followed, is perhaps one of the greatest examples of irrational behavior in the world of finance, at least in recent memory. And for those of you that are interested there is a great book by Michael Lewis titled The Big Short that tracks the story of investors who sensed the crash was coming and made a lot of money with this information.

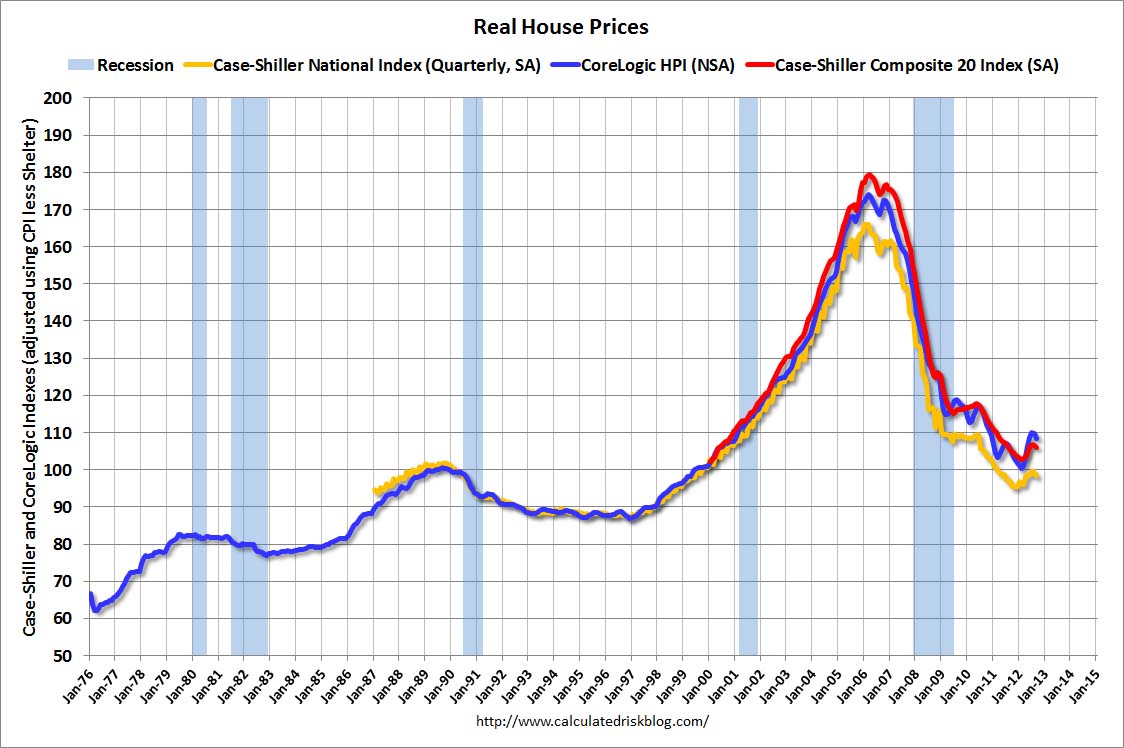

So first we’ll look at how the housing bubble formed. Here is a chart (not mine:http://4.bp.blogspot.com/-NlOkaaw5xS8/ULTxsOcBRgI/AAAAAAAAWgA/Wu-R7NQO7GY/s1600/RealHousePricesSept2012.jpg ) of historical housing prices going back to 1976. It is immediately apparent that prices rose significantly in the early 2000’s, only to see a marked decline beginning in 2006. This graph alone is enough to make one wonder what could cause such a rapid increase in the price of homes? The answer it turns out is human irrationality.

I won’t get into an argument of who's at fault for the bubble, and consequently its burst, instead I will just tell the story and allow you to draw your own conclusions of where the blame lies.

Throughout the 90’s and early 2000’s mortgage application credit standards became increasingly lax, and people with less than ideal credit scores were allowed to purchase increasingly expensive homes. As a result, the rate at which people began buying homes also increased, and so to keep up with the demand more and more homes were built. The increased purchasing and demand for homes naturally caused an increase in the price of homes and all of these factors began to reinforce one another.

In the early 2000s what are known as adjustable rate mortgages became increasingly popular. Adjustable rate mortgages were designed such that for the first few years after a purchase, the homebuyer would pay a very low introductory interest rate that would promptly rise to a more normal rate after the introductory time period was up. With such low mortgage payments, many people felt wealthy - and began spending and buying...a lot

Things got to such a point that some people were buying second or third or even fourth homes counting on the fact that in a few years the value of the house would rise and they could sell to someone else. And for some people this worked splendidly. But then those attractively low introductory interest rates began to expire, and suddenly people could no longer afford their mortgage payments. Just like that the demand for houses dried up; there were more people looking to sell than buy. Housing prices were now rapidly falling as less and less people had the money to buy a third or second or even first home.

This would go on to be called the housing bubble and its burst sent ripples throughout the rest of the economy. After all if people couldn’t afford their mortgage payments how could they afford to buy anything else? To make matters worse, there was a great deal of money invested in housing mortgages. When homeowners could no longer pay their mortgage, the investments in mortgages went bad and many funds lost a great deal of money, leading to a market crash.

I bring up the story of the housing crisis because it is a perfect example of how bubbles form in the stock market. Almost the same exact thinking applies in a stock market bubble: that is, as people feel wealthier and more confident, they are willing to spend more of their money. And this lax attitude allows prices to rise very high very quickly. Eventually these bubbles burst and those who bought at the peak or waited to long to sell are the most affected.

Don’t allow yourself to be caught in a bubble. Force yourself to take a step back from time to time and think about what you are buying and why. As silly as it sounds you might actually have been motivated by peer pressure when you made a decision and not even realize it. And in the financial world it is extremely important to make logical, thought out decisions rather than simply following the herd mentality. All it takes is one small shock to scare the herd into running the other way.

- Determine Risk Appetite for Investing5:16

Risk Appetite and How it Affects Your Decisions

I personally tend to invest in stocks that are considered risky. But your personal appetite for risk might be different from mine. So I’d like to take a moment to help you figure out your risk appetite.

High-Risk

You are comfortable with the possibility of day-to-day price swings of 5%+

You can stomach buying a pharmaceutical stock before the FDA has approved the company’s leading drug candidate, knowing that if the FDA does not approve the drug, the company could be worthless

You are willing to buy stocks with little to no dividend or earnings.

Moderate-Risk

You will only buy companies with historically stable day-to-day prices (i.e. avoid large swings in favor of steady movements)

You will only buy companies that are currently selling a product to consumers

You prefer stocks that have dividends and/or positive earnings.

Risk-Averse

You prefer to keep your money out of the stock market in favor of fixed-income instruments

These categories are not all encompassing and some of you will be in between somewhere, they are just to help you get an idea of how much money you can stand to lose. It’s also important to realize that there is always some level of risk when you invest, even if you choose what are considered to be safe investments. Before the housing crisis, investments in housing mortgages were considered to be among the safest you could choose from.

I am guessing most of you watching this video identify with one of the first two categories, but if you identified as being risk-averse, that’s okay too. I hope that by the end of this course you have the confidence you need to start investing.

As I said I tend to gravitate towards the higher-risk stocks simply because they offer the greatest return potential. But I have been known to buy into safer dividend paying stocks if I find one that appears to be undervalued. And that’s really what successful investing is all about: finding great deals that other people didn’t see.

But why is it so important to know your risk appetite? Well it can prevent you from making rash decisions in the heat of the moment. Someone with a high-risk appetite can likely handle seeing their shares drop 20% better than someone with a risk-averse appetite. The person with the risk-averse appetite is more likely to sell their shares to cut their losses as soon as possible, whereas the person with the high-risk appetite is more likely to give the stock a chance to recover its losses. And so it is extremely important that you are able to accurately identify how tolerant to risk you are because selling a stock just because the price has dropped is a bad decision. What you should really be doing is figuring out what caused the price drop. And this is an area where being able to read into the validity of market-talk can be very helpful.

For instance, it is not uncommon for someone to write a baseless article about a company with the sole intention of affecting the price. All it takes is for one headline to say “Apple is a bad investment!” and there investors out there who will sell after just reading the title. Does this make any sense? Of course not! We haven’t even found out why the article claims Apple is a bad investment let alone if the article’s argument is credible. Maybe the writer simply wanted to convince people to sell the stock so he could buy it at a better price. This sort of manipulation, though technically illegal, is a factor in today’s markets. But the smart decision is to hold onto your shares of Apple, because you’ve read the article and realized everything the writer claims is nonsense.

On the other hand, maybe there is a perfectly valid reason for the stock price to have moved. Maybe Apple has announced its newest iPhone is a complete flop! In which case you should not sell, but should begin to consider the possibility of selling. And I specifically say, “consider selling” because you should never make a buy or sell decision based solely on a single piece of news. Maybe the reason Apple expects its iPhone sales to perform poorly is because customers are instead buying far more iPads than expected! It is important to dig into any and all news pieces, and determine not only their legitimacy, but also whether or not they mean something bad or good for your shares. It’s quite possible that the iPad selling more than expected will cancel out the iPhone’s underperformance! And there are many cases where a particular announcement at first looks like great news for a company, but actually turns out to have a negative effect on shares, and vice versa.

When you are reading market news and doing your stock research, you should never just take something at face value. There is always another viewpoint to consider, and you have to force yourself to think of every viewpoint you possibly can. If you find yourself reading a lot of articles that suggest a particular stock is a buy – take it upon yourself to find and read articles that argue that stock is in fact a sell. You must be open to any and all commentary and simultaneously decide what is a credible argument and what is not. Only then can you say you have made an informed decision.

Not only will this way of thinking help you uncover good investments, it can also turn a risk-averse individual into someone who is comfortable taking on more risky investments. The more you know, the more money you will make.

- Tempering Investment Expectations3:25

Tempering your Expectations

I feel that it is really important to make a video about tempering your expectations because many new investors jump right in hoping to get rich quick. This is not and never has been the case. Money earned from investing is not made in an instant but rather over time, and I want to stress this point because there are many investors who succumb to their lack of patience.

In previous videos I spoke about the yearly average return of the markets being roughly 12%, and I showed you how much money your investments can add up to over the years. The key thing to remember here is that you are investing for the long haul. And even a single year can seem like a long time. And it takes tens of years in a row for your money to grow into a large amount.

Lets go back to the scenarios we looked at for people that started investing at different ages:

It is clear that the earlier you begin investing, the better off you will do. And for some people, this notion of slowly growing your money over time just doesn’t quite sit right. And so I’d like to make it very clear that successful investors have incredible patience. They realize that an investment today doesn’t make them rich tomorrow, or even a year from now. Investing makes you rich 10, 20, or 30 years from now.

If you go place $5,500 into your IRA today, you absolutely must be comfortable with the fact, that that number might only be $5,501 tomorrow. Or it might even drop down to $5,499, or any other amount. But you must realize that the a single day means nothing in the grand scheme of things, because it is only over time you can expect your money to grow into large amounts. In order to earn a 12% return in a year, your money must only grow at an average of 0.03% per day. My point is, do not watch the price of your stocks on a daily basis and think to yourself “ this is taking too long! I don’t have the patience for this!”

Another thing I’d like to bring up is the daily fluctuations in price of both individual stocks and the markets as a whole. The market is a turbulent place, and sometimes the Dow Jones is up 150 points one day, and down 200 points the next. Learn to trust in the decisions you have made in what companies to invest irrespective of market behavior. Price fluctuations should not affect your decision making, because remember: you are in this for the long haul. The only thing that should affect your decision-making is your research and any new news concerning your stocks.

I have a goal that I plan on reaching many years from now. And one of the ways I plan to achieve that goal is through investing in the stock market. I have had to learn about the markets and investing. I have had to research companies to invest in. And most of all, I’ve had to sit and watch my stocks grow once I’ve made a final decision. And this can be the most difficult part for new investors. You’ve made your decision to invest in companies A, B, and C, now what?

Well now you must continually track anything that could affect your stocks. But you most certainly will not buy or sell based on daily price fluctuations. Because you know that through your hours of research, Stock A is selling for half of what it should be, and you are confident that the market will one day value it appropriately. And when that day comes, you will be rewarded for your patience.

As they say, Rome wasn’t built in a day. The same logic applies to your 401k, IRA, or brokerage account.

{kind=link}

- Maximize Return on Investment11:06

Narrowing Your Search

Your portfolio is only as good as the research you’ve conducted. So I’d like to now begin taking you through the process I go through when I look for stocks to invest in – as I imagine that’s the main reason many of you have chosen to watch this series.

It is, unless you have all the time in the world, unfeasible to conduct research on every single company out there – there are just too many companies and not enough time and resources. And so we must find reasonable ways of narrowing down a list of stocks to research. For starters, completely ignore penny stocks altogether. Penny stocks are literally companies that trade for pennies a share (or thereabouts). They also are called over the counter stocks (OTC) and are essentially unregulated. It is unfortunate that we live in a world where people attempt to defraud others, but in the land of penny stocks this is not at all a rare occurrence. And due to a lack of regulation, any losses you may suffer from illicit acts are permanent. If you see the symbols OTC or OTCBB anywhere, you are looking at a penny stock. Buying penny stocks is akin to gambling; forget they exist if you are serious about investing.

So with that warning fresh in your mind lets begin talking about the stocks you actually want to spend your time on. I’d like to first discuss the different stock sectors out there. Fidelity.com provides a lot of good research material on top of their market data and is a website I frequently visit. They list the different sectors as Consumer Discretionary, Consumer Staples, Energy, Financials, Health Care, Industrials, Information Technology, Materials, Telecommunication Services, and Utilities.

Right off the bat I will focus on stocks within those sectors that have shown, or show the potential for the most growth. Generally speaking, I ignore Consumer Staples, Energy, Industrials, Materials, and Utilities and focus on financials, health care, and information technology as I feel they offer the greatest opportunity for gains. In particular, the biotechnology sub-sector of healthcare is one that I feel is unmatched towards generating massive gains in a short time.

To help you better understand my thinking behind these decisions, I’d like to briefly explain the reasons for why I generally ignore or focus on certain sectors.

Sectors I discount:

Consumer Staples: Think of this as the necessities sector, it consists mainly of food and drug retailers and distributors, and companies that sell essential personal products that people cannot live without (think cigarettes, toothpaste, etc.). Companies in this sector are known for their consistent performance in spite of how the broader economy is performing. If the economy is particularly bad these are some of the safest companies to invest your money. However, they are not known for beating the market or even breaking even with the market over the long haul. For example, according to a chart fromFidelity.com, as the S&P has produced returns of 15% over the last year, the Consumer Staples sector has produced gains of only 7% - less than half. Your chance of beating the market with this sector is low.

Energy: This sector is pretty self-explanatory, it consists of companies in the business of producing energy; from drilling for oil to transporting coal on a train. Like Consumer Staples stocks, energy companies are considered safe investments. No matter what the picture of the broader economy looks like, people need to drive to work. I’m a big proponent of the need for green energy sources but realistically fossil fuels are here to stay in some form or another for quite some time. Companies in this sector have very high infrastructure and overhead costs and as oil gets harder to drill for, and as restrictions on emissions get tighter this will only increase. The energy sector is typically one of the lowest performing sectors and your chances of beating the market here are low.

Industrials: This sector consists of businesses involved in the construction and engineering of large industrial projects - anything from defense contractors to airlines to large machinery. This sector does particularly well in times of war but in general will follow the markets ups and downs. You aren’t too likely to find multi-baggers here.

Materials: The materials sector contains companies that are in the business of raw materials. Those companies that mine for metals and minerals, manufacture chemicals, chop down forests etc. Think of the materials sector as the sector that provides all of the building blocks for other sectors to use in the making of their products. Materials companies often have high infrastructure costs, high processing costs, and high transportation costs. These businesses are essential to the economy but they’re profits depend on steady demand. This is not a market-beating sector.

Utilities: Like the energy sector, there is not a lot of money to be made here compared to other sectors. Utilities consist of the companies that distribute power, gas, and water. These companies are here to stay but they don’t make a lot of money for investors. There aren’t many things utilities companies can do to innovate and grow their profits. So I recommend also staying away from this sector.

Sectors I concentrate my research:

Financials: Financials are those companies that are in the business of making money. Whether they hold it for people (banks), invest it for people (investment advisors), or allow consumers access to their money anywhere and everywhere (credit cards). Financial companies are literally where the money is. The potential for profits in the finance sector is huge. In addition, this sector is perhaps the best area to invest in AFTER a financial crisis. Following the bottom of the market crash in 2009, banks have been some of the best performing stocks available, with smart investors earning anywhere from 3-5 times their money in just as many years. That being said, these companies are particularly sensitive to economic catastrophes, with the housing crisis of a few years ago being the most recent example. Caution is advised when investing in this sector but profit potential is high.

Healthcare: With the average lifespan ever increasing, the demand for new drugs and therapies to treat our growing ailments is more and more becoming a pressing need. The healthcare sector includes companies that produce and supply medical equipment/devices, offer health care services (think at-home nurse), and research and produce new drugs and therapies. I focus my investing mainly on those companies in the business of researching and developing new drugs: the pharmaceutical and biotechnology companies. There are numerous diseases within the population that are either insufficiently treated or not even treated at all. And when a pharmaceutical company is able to develop a new drug or therapy to correct this, they are often awarded a patent on their treatment. Earning a patent gives a company the exclusive rights to sell their new treatment for a certain number of years (i.e. a monopoly). It is not uncommon for shares of a biotech company to increase many times over after receiving an FDA approval, or even just announcing positive results from a clinical trial. Here’s an example:

On October 1st, 2012, Sarepta Therapeutics (SRPT) closed at $14.99 per share. Just a few months earlier it had been trading below $4. Then on October 3rd, 2012 the share price closed above $37. So what happened? Well, in July of 2012 the company announced they would be finishing up their Phase 2 trials of their leading drug candidate, a potential treatment for people with Muscular Dystrophy later in the year. The market for a treatment to treat the disease is estimated to be in the billions of dollars. And so investors began slowly buying in the months that followed in anticipation of positive results. And on October 3rd, Sarepta Therapeutics announced positive results – that is there was evidence to suggest that their drug was able to treat Muscular Dystrophy.

The stock went from sub-$4 per share to $37 per share in just a few months – a huge gain by any measure. And I’d like to add that the drug hadn’t even been approved yet, they still would have to conduct phase 3 trials for their drug, a process that would take at least another year or two, before they could even petition for FDA approval. And so you can see that it is extremely advantageous to invest in biotech companies shortly before they announce positive trial results.

Word of caution: biotechs are high risk/ high reward, and that’s why doing careful research is so important. You cannot simply invest in stocks like this on a feeling or a whim. It’s important to carefully research the science behind the ideas. For example, there are frequent cases of companies proclaiming a “stem-cell treatment breakthrough” or a “new state-of-the-art cancer treatment”. Sometimes these are credible, but often they are just news headline fluff or the science is far too difficult to understand. In my opinion and experience, there is an advantage to sticking with companies developing treatments that someone without a PhD can understand.

Information Technology: Computer hardware, software, and Internet companies make up the bulk of the information technology sector. This is the sector where you’ll find the Googles and Microsofts of the world. I think it goes without saying that there is a great deal of money to be made here. And similar to the healthcare sector, this is one of the fastest growing and most innovative areas of the economy. These companies are in the business of meeting our unmet needs through technology and the successful ones tend to be incredibly profitable. This sector consistently beats the market.

I have not yet mentioned the Consumer Discretionary and Telecommunications sectors. The reasons for this are simply that I do not believe I have enough experience to speak about their potential for investing opportunities. I will instead give a brief overview of them and let you decide if you wish to divulge further into these industries.

Consumer Discretionary: This sector refers to companies that sell goods that are not necessities. Think of these as luxury goods companies. I would guess that these companies perform poorly when the broader economy is in bad shape as they depend on consumers having extra money to spend. I cannot however, speak from experience as to what types of market conditions they do well in, and where the best/worst opportunities arise in this sector.

Telecommunications Services: If you have a cell phone, cable TV, and/or Internet access, a telecommunications company is serving you. These are the companies that physically provide the electronic and wireless signals you receive when you make a phone call or surf the web. I have shied away from learning about this sector because I have always viewed it as a utility and assumed that profits for investors would be small. Whether or not this is a correct assumption I cannot say.

So I hope I’ve given you an idea of where to begin your search for great investments. In the upcoming videos I’d like to focus on how to pick stocks from within the high-potential sectors.

- Understand Price to Earnings Ratio of a Stock5:55

What does the P/E Ratio tell you?

Even after we’ve narrowed down our search to a few sectors, there are too many companies within each sector for a single person to analyze in depth. And so there are techniques you can use to help you identify stocks that might be worth your time to research further.

One of the tools I use to eyeball whether I should spend time researching a stock is the Price to Earnings Ratio, P/E ratio for short. Please heed my advice when I tell you to never invest in a stock based on the P/E ratio or any other single indicator alone. With that said, the P/E ratio can give you a rough idea of what the market thinks of that particular companies future prospects.

Mathematically the P/E ratio is simply the price of the stock divided by the earnings per share (EPS). The ratio is used to compare how stocks are priced compared to their peers. And so when we look at P/E ratios, what we are really doing is comparing a single P/E ratio to the other P/E ratios out there. Usually this is done for companies within the same sector or line of business.

So for example if Google were priced at $1000 and its earnings per share were $50 – then dividing $1000 by $50 gives us a P/E ratio of 20. So now we might look at another technology company, lets say Apple. Maybe Apple is priced at $500 and its EPS is $45. Dividing $500 by $45 gives us a P/E ratio of about 11.

So really what does this tell us when we compare the two? Well it essentially tells us that investors in the market are willing to pay a higher price for shares of Google than they are for shares of Apple per every dollar of earnings. This is where you should start to ask questions. Why is it that investors will pay more for Google than Apple? And for this example the reason it is likely that investors think Google has better future growth opportunities than Apple does. So if we were able to project the future revenues and profits of both companies, based on say, expected future sales, we could get an idea of which company stands to make more money. It turns out that the market does not always price shares appropriately, and this is where we look for opportunities.

If for instance, we have two companies in the same line of business, lets say they both sell shoes, but one company is selling for twice the P/E ratio of the other, we would want to investigate why this is so. Is one company significantly better at selling shoes than the other company? Or has the market simply overvalued Company A and undervalued company B? These are questions you want to ask yourself when you look at the P/E ratio indicator.

Again, the P/E ratio absolutely does not tell you which companies you should invest in, it tells you which companies you should perhaps research further if they have an abnormally lower or higher P/E relative to similar companies in their sector.

Some notes about the P/E ratio:

·It is often, but not always the case that very large and mature companies have lower P/E ratios than smaller and younger companies. This can be attributed to the size and growth potential of the companies. Often times, a very large company such as Microsoft does not have large opportunities for growth, but rather maintains a steady and consistent market share. On the other hand, a less mature company that hasn’t achieved its full potential, take Amazon for example, has a much higher P/E ratio because investors are counting on the fact that one day in the future, Amazon will make far more money than it does today. As of the time of this writing Microsoft’s P/E is 13.9, a very typical valuation for a company of its size. Amazon’s P/E is 605.7, suggesting that investors expect substantial earnings growth in the future.

·Typically the ‘E’ in the P/E ratio, is calculated by summing the last four quarters of earnings for the company, this is know as a trailing P/E ratio. And so one particularly good or bad earnings number can skew the ratio. Some websites will instead estimate the expected earnings of the next four quarters. This is called the forward P/E ratio and is essentially an educated guess. When researching stocks it is good to check if the site you are using calculates trailing or forward P/E ratios.

·There is another problem with the P/E ratio that arises with the ‘E’ portion. There are a number of accounting tricks companies can use to alter the quality and appearance of a particular quarter’s earnings, and there are many companies that do use these tricks to their advantage. This is perhaps the best argument for not relying solely on a P/E ratio when making an investment decision.

In summation, don’t let the P/E ratio trick you into making bad decisions. It should only be used to as a tool that makes you ask questions:

·Why is Company A’s P/E ratio higher or lower than Company B’s?

·Is it possible the market is over or undervaluing Company C’s worth?

·Is there any reason to think Company D’s P/E ratio is skewed one way or the other?

Ask yourself these and any other questions you can think of and you may discover a piece of information that the market is overlooking. If you’ve learned everything there is to know about a company and the valuation still looks funny, there is a chance that the market is missing a piece of the puzzle.

It is also good to be aware of the Price to Sales Ratio (P/S) and Price to Book Ratio (P/B). They are similar to the P/E ratio in that you are comparing the share price of the stock to a particular value. Most people, myself included, don’t pay these two other ratios much attention because they are affected by too many variables and therefore not particularly useful for stock valuation. I bring them up here only because you are likely to see the terms in the course of your research.

- Calculate Textbook Stock Valuations7:18

Textbook Stock Valuations

So you might be wondering how investors actually agree on what is a fair price for a stock. The textbook method for stock valuation requires that you gather some information about the company’s cash flows. There are really only two ways of doing this. I will give an overview of both methods before doing some examples.

The first is the Dividend Discount Method, which seeks to calculate the value of a stock based upon all of its future dividend payments. This method requires that the company in question pay dividends. This can be a problem because many companies in fact do not pay dividends. So in order to calculate a stock with this method, you must first check if the company pays a constant a dividend. I place emphasis on the word constant because some companies will pay out a one-time-dividend and a single dividend cannot be used to effectively value a company’s worth. It is recommended that you make sure the company’s dividends are growing as well. The general formula for this method is:

where ‘P’ is the calculated share price or what the company should be worth, ‘D’ is the expected value of next years dividend (the sum of the next four quarter’s dividends), ‘r’ is the cost of equity, and ‘g’ is the growth rate of the dividend. Don’t worry if this is confusing at first, we’ll go through an example in just a moment.

The second way to value a stock is the Discounted Cash Flow Method. And the advantage of this method is that it is not required for the company to pay a dividend to calculate it. But there is a problem with this method as well. It is common for start-ups and young companies to spend all their money on further growing the company. This means the company’s cash flows may be negative for some period of time. In cases such as this the Discounted Cash Flow Method becomes irrelevant. So to value a company using the DCF method, you should check that the company’s cash flows are positive. The formula for the DCF method is:

where ‘CF’ stands for the cash flow of a particular year, ‘r’ is the required return rate (cost of capital for example), and ‘i’ is the year of the particular cash flow.

An inconvenience that arises here is that, as ‘i’ the number of years grows larger, the calculation becomes more tedious.

And so alternatively we can calculate the DCF in perpetuity using the formula:

where g is the average growth of cash-flows each year and r is the cost of capital.

As you can see, the dividend discount method as well as the discounted cash flow method tend to require very specific conditions and assumptions. The problem with these methods is that they seek to oversimplify the worth of a stock. There are so many different scenarios that in reality you will likely have to come up with a variety of ways for valuing companies. I will touch more on this later but first lets go through some examples on how to use the two valuation methods described above.

For the dividend discount method we will start by choosing a stock that not only consistently pays dividends each quarter, but also has shown steady growth of those dividends over the years. Over the last 3 years, the Coca-Cola company has paid a dividend each and every quarter as well as displaying consistent growth of those dividends. To calculate the companies expected worth, that is what the price of the stock should be, we must gather the sum of the next four quarter’s dividends ‘D’, the average growth rate of the dividend ‘g’, and the cost of equity ‘r’. The first 3 variables are fairly easy to calculate.

By looking at the total dividends of each of the last 3 years, we can calculate an average growth of about 4.075%. And we will use this average to estimate next year’s dividend.

Year

2011*

2012*

2013*

2014

Dividend

$1.92

$2.01

$2.08

$2.16 (est.)

Growth

N/A

4.67%

3.48%

4.08% (est.)

*Data from Yahoo! Finance

So now we have our D = $2.16, and our g = $4.08%. All that’s left is to calculate ‘r’.

To calculate our cost of equity, r, we must introduce another formula, the Capital Asset Pricing Model, CAPM for short. The formula goes as follows:

where, rf is the risk free rate (usually the rate of inflation), β is the beta of the stock (can be found on any finance website), and rm is the market rate (the average return of the market). Historically, the inflation rate has been about 3%, so we will use that as our rf. From Yahoo! Finance, the beta of Coca-Cola is 0.34. And we will use the historical market return of about 12% as our rm. Putting this altogether we calculate our cost of equity ‘r’ to be 6.06%. Now we have everything we need to estimate the value of the share price of Coca-Cola:

So the dividend discount method suggests to us that the worth of a share of Coca-Cola AND all of its future dividend payments is about $109.09 per share. I am not by any means suggesting that you go out and buy shares of Coca-Cola; this was merely an example using rough calculations. Also note that this method is very sensitive to changes in any of its variables. If Coca-Cola all of a sudden decides to not pay a dividend next year, this model will suggest the stock is worthless, which is not the case by any means.

For comparison’s sake we will now use the Discounted Cash-Flow method to calculate the value of Coca-Cola shares. For simplicity’s sake, we will calculate the DCF out to 3 years in the future, and then use the perpetuity formula to calculate past those 3 years.

We will need to calculate the average growth of the cash-flows of the Coca-Cola company. We can do this by looking back at the cash-flows from the most recent years and determining on average how much they have grown.

Year

2011*

2012*

2013*

2014

2015

2016

FCF

2.25B

3.27B

3.02B

3.51B

4.07B

4.72B

Growth

N/A

45.3%

(7.55%)

16%

16%

16%

We’ll use our cost of equity from the previous example of 6.06% for ‘r’.

And so to finish the calculation we must determine the value of the cash flows of all the years past 2016 using the perpetuity formula using the historical rate of inflation of 3% for ‘g’.

If we add these two numbers together we can see that our DCF calculations value the Coca-Cola Company at $169.75 billion. On a per share basis this equates to $38.49 per share. For comparison, the current share price of Coca-Cola is $38.20 at the time of this writing. So by the DCF method it seems that the market is valuing Coca-Cola appropriately.

Again, I’d like to clarify that both the Dividend Discount method and the Discounted Cash-Flow method are highly sensitive to small changes in the numbers we are using. Therefore, someone with different growth rate projections could value the Coca-Cola Company very differently than we have here.

Once again, I personally do not rely on either of these methods to value stocks as I feel that they are somewhat arbitrary. But I have chosen to discuss them because they are considered the textbook methods of valuing shares of a company and they may reflect the market’s perception of a company’s worth.

- What is the Worth of a Stock?4:06

What is the worth of a stock?

In the previous video, we went over what are considered the textbook methods for valuing a stock; the dividend discount method and the discounted cash-flow method. And I left off by saying that performing these calculations can give you an idea of what the market perceives a company’s value to be. If the market; that is other investors, fail to do a good job at pricing a particular stock, then an opportunity has arisen for us to take advantage of.

I’d like to remind you how specific the conditions must be for us to apply valuation methods such as the dividend discount and the discounted cash flow. The former requires that a company pays a dividend, and the latter requires that the company have positive cash flows. And in both cases, it is preferable that the company in question be both mature and steadily growing.

The problem with these valuation methods is that the market is littered with companies that don’t meet any or all of these conditions. Take for instance small pharmaceutical or technology companies. Not only do they not pay dividends, they often lose money for many years on end. These companies are focused on spending a lot of money upfront with the intent that down the road their product will be a goldmine. And because there is no agreed upon consensus on how to value stocks like these, they are often the ones with the largest opportunities for gains.

One of the things I look for in a company is profit potential; that is how much money do they stand to make if Scenario A happens, what if scenario B happens, etc. Profits and revenue are the meat and potatoes of any company. And so in the absence of profits, we can instead take an educated guess as to what the profits might be ‘X’ number of years down the road. This is useful to do for any company, but for many companies, it might be the only way of coming up with a valuation.

Short example: A biotech company is developing a drug to treat Rheumatoid Arthritis better than the currently available options. Our first step would be to find out the size of the Rheumatoid Arthritis market. This can literally be done through a Google search assuming you check multiple sources and verify the accuracy of the numbers. You’ll then want to figure out how much market share the new drug could potentially treat if the FDA approves the drug. This is much trickier and there is no one-size-fits-all method so you will have to be creative. For the purposes of this example, I might start by researching how many patients are currently undertreated; that is either they are not treated at all, or their current treatment is insufficient. And perhaps the undertreated are the most likely to use this new Arthritis drug, but that does not mean every or even most of them will. Once we have come up with what we consider to be our most accurate projection for the revenue of this new drug, we can then begin to formulate valuations.

Of course, this is all for nothing if the drug isn’t approved. In the case of a biotech company developing a drug, you will have to estimate how likely it is the FDA will approve the drug. The best place to start is by looking at the companies past trial information. Did the drug display effectiveness over a placebo? What was the dosage? Were side effects reported and if so, what were they? Are these side effects related to the size of dosage?

You must ask yourself as many questions as you can when conducting your research.

The point I am trying to make is that you need to know a company inside and out to make an investing decision. And the opinion you formulate needs to be your own. Too many investors are swayed by the cheap words of columnists and television analysts. If you want to know the worth of the stock, the reality is that you need to expend time and energy. It is much easier to listen to someone touted as an “investing guru” but I can almost guarantee you won’t make money that way. Only you have your best interests in mind.

- Mom! Buy This "Social" Media Company!5:29

Thank you for watching episode one of "Mom! Please Buy This Stock!"

I'll talk about stocks my mom should buy now. Today, we'll talk about $SNAP Snapchat.

We should not compare Snapchat to Facebook, because $SNAP is not a social media company. Therefore, we should compare them to CBS.

If we do that, CBS has a market cap of $21 billion, with annual revenue of $14 billion. CBS also only has 9 million daily active viewers.

Snapchat on the other hand, will not beat Instagram, but that's okay, because they're still worth money. $SNAP has 188 million daily active users and a market cap of $8 billion.

Once Snapchat stops trying to grow their front line revenue, and start to properly monetize on their 188 million users, Wall Street will appreciate $SNAP.

Mom, if you're listening, please buy more $SNAP at $6.90!

Love,

Matt - Mom! Buy This Pharmaceutical Company!4:24

Thank you for watching! I'll talk about stocks my mom should buy now.

Today, we'll talk about $PFE Pfizer.

Recently, Pfizer received FDA approval for three products, for lung cancer, breast cancer, and preventing viruses from chemotherapy.

More importantly, $PFE has revenues close to $53 billion per year with $21 billion in profit and a price to earnings ratio of only 11.79. For a healthy stock, P/E ratio should be between 15-18.

Therefore, if $PFE had a P/E ratio of 15, they'd have a $56/share price. It's that simple mom!

Mom, if you're listening, please buy more $PFE at $44.00 and collect their 4% dividend on the way up!

Love,

Matt - Mom! Buy This Telecommunications Company!5:32

Thank you for watching! I'll talk about stocks my mom should buy now.

Today, we'll talk about Verizon $VZ.

Verizon has 103 million wireless users, with a revenue of $126 billion per year and net profit of $30 billion! They have a market cap of only $240 billion.

In theory, my mom could invest in Verizon today, and in 9 years, they'll double their market cap through pure profits.

Right now, their P/E ratio is only 7.5. $VZ is a healthy company that makes $30 billion per year. Not many companies can say that.

Therefore, they should have a healthy P/E ratio of 15. Right now, they have massively undervalued. Their stock price should be about $115, not $57.

Facebook has one of the biggest audience to advertise to, but Verizon actually isn't that far behind. They own Yahoo! which has over 1 billion monthly users. AOL with almost 200 million, Huffington Post with 100 million, and many more companies. This allows Verizon to also collect user data and advertisement revenue, much like Facebook!

Mom, if you're listening, please buy more $VZ at $57.00 and collect their 4.2% dividend on the way up to $115.

Love,

Matt - Mom! Also Buy This Telecommunications Company!3:51

- Mom! Please Buy This REIT!3:21

- Mom! Buy This Car Company!2:54

Requirements

- There are no prerequisites although would be good to consider your long-term financial goals.

Description

Join 20,000+ students in a best-selling complete stock investing course on Udemy!

Introduction:

Hi, my name is Matt Bernstein, successful Udemy instructor with over 175,000+ students across 198 countries.

From an investing standpoint, my most successful investments in 2008 were, Google and Apple. In 2012 they were, Facebook, Tesla, and Netflix. Most recently, investing in Twitter at $14.50 in 2017. Check my Quora account if you don't believe me ;) Which, I was a top writer in 2017.

In this course, you'll discover great investment to make in 2018 and 2019!

Description:

Investing in the stock market can be mastered by anyone and for those who really learn the key concepts and best practices they will be more prepared for retirement.

Unfortunately, many people do not receive the key educational information and best practices that make the difference between success and failure when investing in stocks.

Not boring theory. You will learn practical tips and best practices from an instructor

No inheritance or luck just good sound actions over the years that you will learn about in the course and can replicate for your own personal situation.

No get rich quick scheme or a course that is designed to sell you consulting services this course has one mission and that is all about sharing of experience and wisdom from a successful long-term stock investor and teaching you how you can apply it to your own goals and time horizon.

Highlights:

Discover and invest in stocks that outperform the DOW and S&P 500.

Maximize your return on investment.

Understand the history of the stock market so you will not be doomed to repeat other people's mistakes.

Decide whether a financial adviser is right for you.

Think rationally about the stock market and think long term.

Determine your risk appetite investing in stocks.

Calculate textbook stock valuations.

Stocks to Buy:

You'll gain access to updated content showing you which are the best stocks to buy now. The video series will be called, Mom! Please Buy This Stock!" because, I am not licensed/certified to give anyone financial advice. Therefore, I'm not telling you to buy anything, I'm telling only my mom to buy it :)

To your success,

Matt Bernstein

Who this course is for:

- The experts agree, everyone should consider investing in the stock market for retirement.

- People who want to learn the most important concepts that are needed to become successful in trading.

- Investors who want to better time their entries and exits to increase their returns.