Your cart is empty.

Keep shopping

Teach on Udemy

Turn what you know into an opportunity and reach millions around the world.

Learn MorePython for Corporate Finance and Investment Analysis

Python for Corporate Finance and Investment Analysis

Introduction to Financial Automation: Empowering Financial Decision-Making Through Python Programming

Role Play

Created byJohn Cousins

Last updated 7/2025

English

What you'll learn

- Learn to manipulate and analyze financial data using Python

- Develop theories about asset prices that are informed by real-world financial and economic relationships, and then rigorously test them.

- Understand the Basics of Python Programming

- Python availability in Excel introduces a fresh realm of possibilities for data analysis that was once primarily accessible to data scientists and developers.

- Gain a foundational understanding of Python programming, including data types, control structures, functions, and libraries essential for financial analysis.

- Acquire the ability to construct financial models and forecasts using Python, including cash flow analysis, budgeting, and financial statement analysis.

- Acquire the ability to construct financial models and forecasts using Python, including cash flow analysis, budgeting, and financial statement analysis.

- Applying the Black-Scholes model, bond yield calculation for options pricing.

- Programming with Python Write effective Python code for solving complex business problems.

Explore related topics

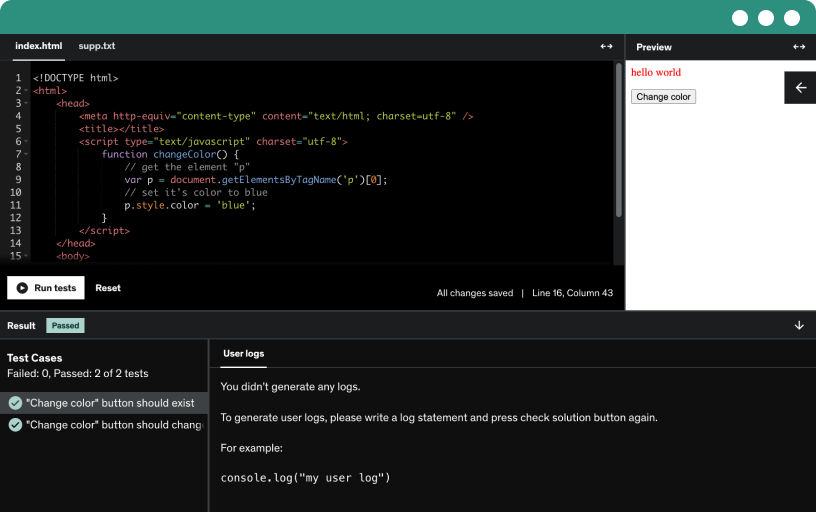

Coding Exercises

This course includes our updated coding exercises so you can practice your skills as you learn.

See a demo

Course content

45 sections • 223 lectures • 11h 28m total length

- Introduction1:56

This course includes many coding exercises in Python. If you don't know computer coding, don't worry, you will get lots of valuable skill set training from this course.

For those of you who have a basic knowledge of Python and coding these exercises will help turbo charge your career.

Integrating Python coding exercises into finance education offers several significant benefits for students. These benefits stem from the increasing role of technology and data analysis in the finance sector. Here are some key reasons why Python coding exercises are beneficial for finance students:Enhanced Data Analysis Skills:

Python is widely used for data analysis and data science. Finance students can leverage Python to analyze complex financial datasets, perform statistical analysis, and visualize data, skills that are highly valuable in today's data-driven finance industry.

Automation of Financial Tasks:

Python can automate many routine tasks in finance, such as calculating financial ratios, risk assessments, and portfolio management. By learning Python, students can understand how to streamline these processes, improving efficiency and accuracy.

Integration with Advanced Financial Models:

Python is versatile and can be used to develop sophisticated financial models for risk management, pricing derivatives, asset management, and more. Understanding these models is crucial for modern finance professionals.

Machine Learning and Predictive Analytics:

Python is a leading language in machine learning and AI. Finance students can learn to apply machine learning techniques for predictive analytics in stock market trends, credit scoring, fraud detection, and customer behavior analysis.

Access to a Wide Range of Libraries:

Python offers a vast array of libraries and tools specifically designed for finance and economics, such as NumPy, pandas, matplotlib, scikit-learn, and QuantLib. Familiarity with these libraries expands a student’s toolkit for financial analysis.

Preparation for Industry Demands:

The finance industry increasingly values tech-savvy professionals. Familiarity with Python and coding in general prepares students for the current demands of the finance sector and enhances their employability.

Understanding of Algorithmic Trading:

Python is extensively used in algorithmic trading. Finance students can learn to code trading algorithms, understand backtesting, and gain insights into the technological aspects of trading strategies.

Improved Problem-Solving Skills:

Coding in Python fosters logical thinking and problem-solving skills. These skills are transferable and beneficial in various areas of finance, from analyzing financial markets to strategic planning.

Broad Applicability:

Python is not just limited to one area of finance but is applicable across various domains, including investment banking, corporate finance, risk management, and personal finance.

Collaboration and Innovation:

By learning Python, finance students can more effectively collaborate with IT departments and data scientists, bridging the gap between financial theory and applied technology, leading to innovative solutions in finance.

Incorporating Python into finance education equips students with a practical skill set that complements their theoretical knowledge, making them well-rounded professionals ready to tackle modern financial challenges.

- I have put some Python materials at the beginning of the course. Check them out:0:32

I have put some Python materials at the beginning of the course. Check them out:

a quick primer,

an entire PDF book on mastering Python,

and an article about how I would learn Python from scratch in 2024.

Also, there are lots of free courses:

Udacity has a great one,

CodeAcademy,

And tons of YouTube instruction.

There are also some great courses here on Udemy.

You can get up to speed in a week or two, and then the coding exercises in this course will help you train up fast by providing bite-sized real-world problems.

If you have any coding training, then Python is easy; it's just formatting, conditional statements, and loops, like any other programming language.

Let me know if this helps and how your journey progresses!

- Mastering Python: a beginner's roadmap2:37

Mastering Python in 2024: A Beginner's Roadmap

As we navigate through 2024, Python has cemented its position as a cornerstone language in data science. With most of the leading-edge machine learning tools written in Python, it's increasingly becoming a staple requirement for data science positions.

Yet, Python's utility extends far beyond data science, permeating various domains of computer science such as:

Web development

Video game creation

Backend system engineering

Thus, for aspiring programmers, data scientists, or those aiming to become proficient developers, Python is a highly adaptable and valuable skill.

My four-year journey with Python has equipped me with insights that I'm eager to share, particularly on how beginners can effectively learn Python from scratch.

Step 1: Course Selection

Initially, I'd seek out a foundational Python course that resonates with me, one endorsed by peers with robust Python expertise. Remember, there isn't a singular "correct" course. While some courses are more esteemed than others, any top-tier course will impart the same foundational knowledge. The key is to commence your learning journey without overthinking the choices.

For instance, I began with the W3Schools Python tutorial, appreciating its simplicity and the practical exercises accompanying each module. While completion doesn't equate to mastering Python, it does provide a comprehensive overview and a firmer grasp of the basics.

What's essential here is commitment. Choose a course and see it through. You'll want to ensure you grasp the following concepts:

Variables and Data Types

Boolean and Comparison Operators

Control Structures and Conditionals

Iteration using For and While Loops

Functions

Native Data Structures (Lists, Dictionaries, Tuples, etc.)

Object-oriented Programming with Classes

Utilizing Packages

This framework is incomplete, as each of these topics encompasses additional sub-concepts.

Step 2: Persistent Practice

There is a saying that I like from Naval Ravikant, a famous entrepreneur and investor, that goes:

It's not 10,000 hours, it's 10,000 iterations.

Echoing Naval Ravikant's sentiment, mastery arises not from mere hours but from iterative practice. This philosophy, contrasting Malcolm Gladwell's "10,000-hour rule," emphasizes the quality and frequency of practice over quantity.

To hone your Python skills, establish a routine that embeds Python coding into your daily or weekly schedule, striving for consistency. Regular engagement can yield significant progress, even if it's just a couple of hours a week.

This course will give your lots of programming exercises to gain proficiency with Python.

Platforms like HackerRank also offer an excellent starting point, presenting a gamut of coding challenges that facilitate rapid learning through problem-solving.

Alternatives like LeetCode and Codeacademy also provide a plethora of problems to solve. There's no set number of problems to tackle; aim for comfort and familiarity with Python's syntax and problem-solving approaches.

Step 3: Embark on Projects

Project-based learning is paramount. It's the synthesis of knowledge where you apply what you've learned to create and troubleshoot real-world applications.

Your project choice should align with your career aspirations. If data science beckons, engage in machine learning or data analysis projects. For web development aspirations, delve into building websites using frameworks like Django.

RealPython offers excellent tutorials and project ideas for budding backend developers and other Python enthusiasts.

Ultimately, the secret is to dive in. Select a project that intrigues you and invest yourself fully into it, focusing on the educational journey rather than the project's complexity.

In Conclusion

Python's ubiquity across various technological realms makes it an invaluable asset for any career in programming. The pathway I've outlined—beginning with a fundamental course, followed by consistent practice, and culminating in hands-on projects—is designed to solidify your Python skills efficiently.

While these steps alone may not instantaneously land you your dream job, they will accelerate your Python learning curve and enhance your ability to apply your knowledge practically. Embrace the challenges and learning process; the effort will undoubtedly pay off.

- Python Primer0:03

Attached is a downloadable document to get you started and familiar with Python.

- The Python Handbook1:14

The Python Handbook

Welcome to the Python Handbook, your comprehensive and all-encompassing guide to mastering one of the world's most versatile and powerful programming languages. Whether you are a seasoned developer looking to expand your skill set or a complete beginner eager to dive into the world of coding, this handbook is designed to equip you with the knowledge and tools you need to succeed.

Python, the language of choice for many industries, is a versatile powerhouse. From web development and data science to artificial intelligence and automation, Python's simplicity and readability make it an ideal starting point for newcomers. Its robust libraries and frameworks offer seasoned programmers the flexibility to easily tackle complex projects, opening up a world of possibilities.

In this handbook, you will embark on a journey that begins with Python programming fundamentals, laying a solid foundation with core concepts such as variables, data types, and control structures. As you progress, you will explore more advanced topics, including object-oriented programming, web development with Django and Flask, data analysis with Pandas, and machine learning with TensorFlow and Scikit-Learn.

Each chapter is crafted to provide clear explanations, practical examples, and hands-on exercises that reinforce your understanding and help you apply what you've learned. You'll find tips and best practices from industry experts, ensuring you learn how to code and write clean, efficient, and maintainable Python code.

The Python Handbook is more than just a tutorial; it's a resource you'll return to repeatedly as you grow your skills and take on new challenges. With this handbook by your side, you'll have the confidence to navigate the Python ecosystem and unlock its full potential.

Prepare to embark on an exciting journey of discovery and innovation. Let's dive into the world of Python and start building the future today!

- Master Python Programming Books0:09

Attached are downloadable PDFs of fantastic books on Python Programming. This course assumes you are relatively familiar with Python, but if not or you need a refresher or reference guide, these books will do it. : )

- Additional Reference Books on AI0:04

Here are some more books that you will find interesting on artificial intelligence, coding, and algorithms.

- AI Algorithms0:40

AI Algorithms Explained

1. Logistic Regression: Predicts yes/no outcomes.

2. Recurrent Neural Networks (RNN): Understands sequences like stories.

3. K-Means Clustering: Groups similar items together.

4. Principal Component Analysis (PCA): Packs important data into a small space.

5. Autoencoders: Compresses and reconstructs images.

6. Neural Networks: Learns from examples like our brain cells.

7. Reinforcement Learning: Learns with rewards, like training a dog.

8. Q-Learning: Finds the best path in a maze.

9. Naive Bayes: Predicts outcomes based on prior knowledge.

10. k-Nearest Neighbors (k-NN): Finds similar items by asking friends.

11. Bayesian Networks: Predicts by considering different factors.

12. Support Vector Machine (SVM): Separates items with the straightest line.

13. Genetic Algorithms: Mixes traits to create the best solution.

14. Linear Regression: Predicts outcomes based on past data.

15. Random Forests: Combines multiple answers for accuracy.

16. Convolutional Neural Networks (CNN): Recognizes patterns like faces.

17. Decision Trees: Makes decisions with yes/no questions.

18. Gradient Boosting: Improves with each small mistake.

- AI Tools0:04

30+ Best AI tools to 10x Productivity!

AI is the future. All should take AI seriously.

- Introduction to Quizzes1:00

I have added a bunch of quizzes to test your comprehension after video lectures. Here is why:

Practice with struggle > practice without struggle.

An example is a study of two groups of students. Group A studied a paper for 4 days. Group B studied it for 1 day and was tested on it for 3 days.

At the final test, Group B scored 50% more than Group A.

Why?

With every test, group B struggled. And that targeted struggle made them acquire more knowledge in the same amount of time.

This is about self-motivation and the measure of self-motivation in a person is the best predictor of upward mobility. Congratulations you have it.

Let me know what you think of the quizzes and this approach.

Cognitively the act of taking a quiz, calling up knowledge from memory, makes that memory stronger and easier to access. So students who are frequently quizzed retain more knowledge of the subject they are studying.

Here are some of the benefits of using quizzes in online courses:

· Retrieval practice occurring during quizzes can greatly enhance retention of the retrieved information. An even higher level of retention than from restudying or rereading the course material.

· Quizzes permit students to discover gaps in their knowledge and focus study efforts on difficult material.

· An indirect effect of quizzes was found that if quizzed frequently, students tended to study more and with more regularity.

· Quizzing has been found to enable better metacognitive monitoring for both students and teachers because it provides feedback as to how well learning is progressing. Quizzes can be a beneficial self-learning check for students.

· Every time a student calls up knowledge from memory like when taking a quiz, that memory solidifies becoming more stable and more accessible.

Quizzes help us identify we know and what we don't know.

Repeated testing with quizzes and exams improves the cognitive process that can amplify long-term memory retention and retrieval. It doesn't just measure knowledge, but challenges it. If you test yourself more regularly, you are going to learn in greater detail than before.

Practice with struggle > practice without struggle.

- Corporate Finance Book download0:05

Attached is my award winning Corporate Finance book. It will help you get familiar with the financial concepts in this course.

- Investing Book download0:06

Attached is a PDF copy of my stock investing book. It will help in covering the capital markets concepts that we explore in this course.

- The Art of Quality Investing0:09

The Art of Quality Investing

This book summary will teach you what you need to know

• An introduction to quality investing

• Checklist to find quality stocks

• Qualitative criteria

• Quantitative criteria

• How to build a portfolio with quality stocks

- Download the MBA ASAP Excel Handbook with Python Section1:43

Python availability in Excel introduces a fresh realm of possibilities for data analysis that was once primarily accessible to data scientists and developers. Now, within the comfort of your well-known spreadsheet environment, you can tap into the capabilities of Python. Check out Chapter 11 "Getting Started with Python in Excel"

Excel is a versatile and indispensable tool for finance professionals. Its importance cannot be overstated, as it is used in a wide range of financial tasks, from data analysis to financial modeling and reporting.

Financial Analysis and Reporting: Excel enables finance professionals to sort, analyze, and visualize data to identify trends, perform variance analysis, and forecast future financial scenarios. It supports using pivot tables, advanced formulas, and various graphing tools, which are crucial for creating detailed financial reports.

Financial Modeling: Excel is widely used for financial modeling, allowing analysts to build models that can predict income, budgeting, cash flow, and other financial projections. Using advanced functions and creating flexible, dynamic models is critical to making informed business decisions.

Excel Proficiency is a Game-changer for finance professionals, significantly boosting productivity by saving time. The ability to automate tasks with macros, handle complex calculations with ease, and manage large datasets efficiently are just a few ways Excel streamlines financial tasks.

Excel is not just a tool; it's a universal language in the finance industry. Mastery of Excel is often a prerequisite for many finance roles, making it an indispensable skill for job proficiency and career advancement.

Decision Making: Excel helps finance professionals in decision-making processes by providing a platform to work through various financial scenarios and analyze potential outcomes. What-if analysis and sensitivity tables are instrumental in this regard.

Accuracy and Precision: Excel's precision in handling financial data is critical. A single error can result in significant financial discrepancies; thus, the ability to use Excel to manage and cross-check numbers accurately is vital.

Integration and Compatibility: Excel can integrate with many business applications and databases, making it an effective tool for consolidating information from various sources for financial analysis and reporting.

Knowing Excel in finance is not just about understanding the basic features; it involves a deep understanding of its advanced capabilities, which are essential in the sophisticated world of finance.

Excel proficiency is a foundational skill that enables finance professionals to perform their roles effectively and efficiently, whether running regressions, building a discounted cash flow model, or analyzing complex datasets.

Download the MBA ASAP Ultimate Excel Handbook and level up your skill set.

- Excel Lookup Functions1:30

Vlookup vs. Hlookup vs Xlookup

Learn the most popular Excel functions and which ones to use when

Lookup functions are REALLY popular in Excel.

Because they allow you to “lookup” a value from a dataset based on the criteria that you enter.

Most people only focus on Vlookup without realizing that there is a far more powerful lookup function called Xlookup.

Let’s explore these three lookup functions and become a pro:

VLOOKUP

How it works → Searches VERTICALLY in the first column of a specified range and returns a value in the same row from a column you specify.

Syntax → =VLOOKUP(lookup_value, table_array, col_index_num, [range_lookup])

Pros →Easy to use for vertical lookups, Supported in all versions of Excel.

Cons → Limited to vertical searches, Searches must start in the first column of the range.

My take → VLOOKUP is probably the most common lookup function, but it’s sooo limited. Learn to ditch this function and focus on XLOOKUP!

HLOOKUP

How it works → Searches HORIZONTALLY in the first row of a specified range and returns a value in the same column from a row you specify.

Syntax → =HLOOKUP(lookup_value, table_array, row_index_num, [range_lookup])

Pros → Useful for horizontal lookups, Supported in all versions of Excel.

Cons → Limited to horizontal searches, Inefficient with large datasets.

My take → HLOOKUP isn’t as popular as VLOOKUP but is very similar. As mentioned above, while this may get the job done, there is a bigger and better option with XLOOKUP.

XLOOKUP

How it works → Searches for a value in an array or range in EITHER DIRECTION and returns a value from a corresponding array or range.

Syntax → =XLOOKUP(lookup_value, lookup_array, return_array, [if_not_found]

Pros → Can search in any direction, Allows for the return of an array, and provides an option for a default value if no match is found, which is very efficient.

Cons → Only available in Excel for Office 365, Excel 2019, and later versions, can be complex.

My take → XLOOKUP solves all the issues that VLOOKUP and HLOOKUP have, and it will gradually take over the Excel lookup universe.

What makes this even more powerful is nesting another XLOOKUP inside your XLOOKUP, which allows you to find the value with both your X and Y axes.

- Bookkeeping A$AP32:03

- Accounting Fundamentals1:02

Accounting is the procedure of data entry and recording, summarizing, analyzing, and reporting financial data. The end product of accounting is the three financial statements: Income Statement, Balance Sheet, and Cash Flow Statement.

FIVE BASIC ACCOUNTING PRINCIPLES:

1: Revenue Recognition:

→ Revenue is recorded at the time of the transaction.

2: Matching Principle:

→ Assets are recorded at their acquisition cost.

3: Historical Cost:

→ Fiscal Year Income is compared with Calendar Year Expense.

4: Full Disclosure:

→ Full disclosure of all relevant info is made available.

5: Objectivity Principle:

→ Information in books should be true, relevant, & accurate.

5 CATEGORIES OF ACCOUNTING:

1: Assets:

→ All Tangible & Intangible items owned by the company.

2: Liabilities:

→ Amounts the company owes to others.

3: Equity:

→ Net Worth of Entity: Assets - Liabilities

4: Expenses:

→ Amount paid purchases made in business.

5: Income:

→ Amount earned by the company from the sale of goods.

JOURNAL VS LEDGER:

→Journal Entries consist of Debits & Credits, the totals of which should be equal

→Journal entries are then transferred to the appropriate Ledger Accounts

FINANCIAL STATEMENTS:

1: Income Statement:

→ Shows profit or loss during the period.

2: Balance Sheet:

→ A company's assets, liabilities, and equity at a point in time.

3: Statement of Cash Flow:

→ Shows the inflow and outflow of cash during the period.

DOUBLE ENTRY SYSTEM

→ Each Accounting Entry will have two sides - Debit and Credit.

THREE FIELDS OF ACCOUNTING:

→ Financial Accounting: Preparing the Financial Statements.

→ Managerial Accounting: Prepare reports for internal use.

→ Cost Accounting: Measure the performance of resources.

- Basics of Accounting0:09

The basics of accounting

This PDF will teach you everything you need to know

Here's what you'll learn:

- Accounting Cycle & Accounting Equation

- List of Accounts and Its Classification

- Accounting Principles

- Journal Entries, Adjusting Entries, & Closing Entries

- Financial Statements

- 13 Accounting Principles1:09

13 Accounting Principles

Accounting is the language of business.

If you want to read financial statements, you MUST understand these 13 principles:

ACCOUNTING PRINCIPLES

→ The rules, benchmarks, and procedures in the accounting field companies should follow while reporting financial statements. In the United States, the common set of accounting standards is GAAP (Generally Accepted Accounting Principles).

ECONOMIC ENTITY

→The Owner & business are two different entities with separate liabilities.

REVENUE RECOGNITION

→ Revenue should be recognized using the accrual basis of accounting.

CONSERVATISM

→When there are two acceptable options for reporting, the less favorable option should be chosen.

CONSISTENCY

→The usage of methods and principles should be consistent until another method proves to be better.

HISTORICAL COST

→Assets should be recorded based on their original purchased value.

FULL DISCLOSURE

→All important information should be disclosed within the financial statements or as a footnote.

GOING CONCERN

→Business is assumed to carry on forever with no intention of liquidation.

MATCHING CONCEPT

→All debits should have a matching credit, and all credits should have a matching debit.

MATERIALITY

→Any information which will have a significant impact should be reported on the financial statements.

MONETARY UNIT

→Transactions that carry a monetary value should be recorded in terms of a monetary currency (Eg, Dollars)

RELIABILITY

→Transactions should only be recorded that can be proven & have significant evidence.

REVENUE TIMING

→ Revenues will be recognized at the time of the transactions regardless of whether payment has been made.

TIME PERIOD

→There should be a standardized time period for the reporting of the financial statements (Ex: Monthly, Quarterly, or Annually)

Do any of these principles need further explanation? If so, let me know in the comments section.

- Tangible and Intangible Assets0:43

???????? ?? ?????????? ??????

This used to confuse me.

There's an easy way to distinguish them.

???????? ?????? ??? ?? ???????

?????????? ?????? ???'?

Here are some other noteworthy differences:

? ???????????? ??. ????????????:

- Tangible assets are depreciated over their useful life.

- Intangible assets are amortized over their useful life.

? ?????????:

- Valuation of tangible assets is generally based on cost or market value.

- Intangible assets valuation often relies on the income approach or market comparables.

? ????????:

- Tangible assets typically have a finite lifespan.

- Intangible assets can have an indefinite lifespan, depending on the asset type.

? ???? ?? ????????????:

- Tangible assets are more risky due to physical deterioration or technological advancements.

- Intangible assets face lower physical obsolescence risks but can be affected by changes in law, market demand, or technology.

? ?????????? ?????:

- Tangible assets are often used as collateral for loans due to their physical value.

- Intangible assets are less commonly used as collateral due to difficulty in valuation.

? ????????

- Tangible assets are acquired or constructed physically.

- Intangible assets are created through legal or intellectual effort.

- Cost Accounting Formulas0:18

Cost Accounting Formulas

This PDF teaches you everything you need to know

Here's what you'll learn:

- Total Cost (TC)

- Average Cost (AC)

- Marginal Cost (MC)

- Contribution Margin (CM)

- Gross Profit (GP)

- Break-Even Point (BEP)

- Return On Investment (ROI)

- Cost of Goods Sold (COGS)

- Overhead Allocation

- Cost Variance

- Price Variance

- Labor Efficiency Variance

- Predetermined Overhead Rate (POR)

- Economic Order Quantity (EOQ)

- Cost of Quality (COQ)

- Production Volume Variance

- Margin of Safety

- Availability

- Reorder Point

- Takt Time

- GAAP vs non GAAP1:02

GAAP vs non GAAP

If accounting is the language of business, as we often teach, understanding its high-level concepts is essential.

Yet, when listening to insiders or stock market veterans, they often use industry jargon and alphabet soup acronyms without explaining what each means.

In today’s lesson, we will tackle one of accounting’s most confusing terms, which is crucial to understand when going through a company’s financial statements: GAAP, which stands for generally accepted accounting principles.

GAAP accounting is a commonly accepted set of rules and procedures designed to govern corporate accounting and financial reporting within the United States.

GAAP rules were jointly established by the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB).

GAAP rules are applied to profitable corporations (overseen by the FASB) and government and non-profit organizations (regulated by the GASB).

This raises an important question: Why do companies report non-GAAP results if GAAP rules are for corporations?

Non-GAAP refers to accounting practices that do not comply with the GAAP standards. As a result, these metrics aren’t audited and don’t have a standardized reporting format.

Many companies report non-GAAP results to shareholders (in addition to their GAAP results) to add important color and nuance to their numbers that the GAAP standard misses.

However, it’s important to note that non-GAAP numbers can also disguise weaknesses in a company’s results.

Therefore, a discerning investor must carefully comb through the numbers, comparing the GAAP with the non-GAAP results, to see an accurate picture of companies’ finances.

- Accouting A$AP22:27

- Financial Statements in 60 Minutes1:39

Welcome to the first section of this course: understanding financial statements.

Financial statements are the end product of accounting. Accounting can seem tedious, but it is the basis of business and investing. Double-entry bookkeeping is 500 years old and is one of the most significant technological inventions ever. The economic development it unleashed fueled the renaissance, the enlightenment, and the modern era.

Johann Wolfgang von Goethe rapturously described accounting this way: “Double-entry bookkeeping is one of the most beautiful discoveries of the human spirit.”

Understanding financial statements are the door to understanding accounting and business.

By the end of this short course, you will understand financial statements and open up a world of potential for your career and life.

You will probably look back over the following years and decades and see this as an inflection point in your destiny.

Download the book here as a printable pdf or Kindle compatible file.

Let’s get started!

Understanding Financial Statements

Financial statements are essential tools that provide a clear picture of a business's or individual's financial activities. At their core, they serve as a report card detailing how money moves in and out.

Income Statement: Think of this like a monthly budget. It tracks money coming in (revenues) and money going out (expenses). The difference between the two gives the profit or loss. For individuals, it's akin to measuring salary against monthly expenses to determine savings.

Balance Sheet: This offers a snapshot of what a business owns and owes at a specific point in time. On one side, there are assets – everything the business owns that has value, like buildings, equipment, or even cash in hand. On the other side, there are liabilities (what the business owes to others) and equity (the owner's share). The fundamental rule is that assets will always equal the sum of liabilities and equity.

Cash Flow Statement: While the income statement might show a profit, it doesn't necessarily represent cash. This statement bridges the gap. It tracks actual cash moving in and out, divided into three categories: money from doing business (operations), money from buying or selling big items (investing), and money from loans or paying back loans (financing).

Business leaders, investors, and banks use these statements to understand a company's health. They help determine whether a business is growing, if it can pay its bills, and if it might be a good place to invest money. Public companies share these with the government for regulatory reasons, and private companies provide them to the government primarily for tax purposes.

- Intro to Understanding Financial Statements1:03

The Most Important Finance Job

The most important set of tasks that a CFO (Chief Financial Officer) has is the oversight, management, and preparation of financial statements. Financial reporting with financial statements happens regularly, at least every quarter and once a year for audited financials. Once you complete a set of financial statements, you are working on the preparation of the next set.

Becoming intimately familiar with financial statements and how they are interconnected and flow is the critical skill set for corporate finance.

Financial statements also underlay Discounted Cash Flow analysis, NPV, IRR, and all the valuation techniques of finance. We will now spend some time thoroughly understanding financial statements.

- Financial Statements Overview Lecture12:10

Intro to Financial Statements

What are financial statements?

The 3 Financial Statements:

Income Statement

Balance Sheet

Cash Flow

Understanding Financial Statements

When you have completed this section of MBA ASAP, you will have a solid understanding of Financial Statements and you will be able to draw meaningful conclusions from their contents. This knowledge can be highly impactful for the quality of your career, job prospects, and life.

Financial Statements are the basic language of money and business. Everyone should have a basic understanding of Financial Statements: what they are and what information they provide. It’s a competency that can open up opportunities and vistas that are closed off otherwise.

Executives like the CEO, COO, and CFO routinely share and discuss financial data with marketing, operations, and other direct reports and personnel within an organization. They also compile and share financial information with stakeholders outside the firm such as bankers, investors and the media.

But how much do you really understand about finance and the numbers? A recent investigation into this question concluded even most managers and employees don’t understand enough to be useful. Check out the quiz in this section to see how you stack up. I will offer the quiz again at the end of the course so you will be able to gauge how your level of financial competency has improved.

Three Main Financial Statements

There are three main financial statements and they are linked together to provide a picture of the financial position and health of an enterprise. They represent the end product of accounting, meaning they are the reports generated by accounting covering all of the transactions of a company.

The three basic financial statements are the

Balance Sheet: which shows firm's assets, liabilities, and net worth on a stated date

Income Statement: also called profit & loss statement or simply the P&L: which shows how the net income of the firm is arrived at over a stated period, and

Cash Flow Statement: which shows the inflows and outflows of cash due to the firm's activities during a stated period.

Knowing how to read and understand financial statements is a business skill you can’t ignore. It can help working your way up the corporate ladder by communicating with others in your company and understanding the big picture. It is also a useful skill in order to understand where your efforts and work can make the most impact.

When you are thinking about possibly changing jobs and working for a company you can check their financials and make sure they are a healthy organization. If you are considering starting your own company you will need to have financials prepared by your accountant in order to talk to investors, bankers and vendors.

If you want to invest wisely in the stock market, analyze the competition or benchmark your performance, you can look up the financials of any publicly traded company at the Securities and Exchange Commission website’s’ EDGAR filings and get an idea of how they are doing. Check out any public company’s most recent 10K filing there. A 10K is the Annual Report of the company and its most important business and financial disclosure document.

Next we will go over each of the financial statements individually and how they are interrelated. You will find lots more information in the books and other downloadable documents that accompany this course.

- Financial Statements A$AP21:38

- Quiz for Financial Statements Overview

- The Income Statement: Revenue6:30

Revenue = profit per unit sold X number of units sold

Pricing power. Charge more.

Silicon Valley legend Marc Andreessen was asked what he would put on a billboard. Marc said two words: "Raise Prices.

The number one thing – just the theme, and we see it everywhere – the number one theme that our companies have when they get really struggling is they are not charging enough for their product. It has become absolutely conventional wisdom in Silicon Valley that the way to succeed is to price your product as low as possible under the theory that if it's low-priced everybody can buy it and that's how you get the volume. And we just see over and over and over again people failing with that because they get in the problem we call too hungry to eat. They don't charge enough for their product to be able to afford the sales and marketing required to actually get anybody to buy it. And so, they can't afford to hire the sales rep to go sell the product. They can't afford to buy the TV commercial, whatever it is. They cannot afford to go acquire the customers."

The Income Statement

The basic structure and components of the Income Statement are reviewed in this section. The Income Statement is sometimes called the Profit and Loss Statement, or P&L for short.

The components of the Income Statement are:

Revenue

Expenses

Net Income

Profit

Earnings

The Income Statement

The daily operations of a business are measured in the money that comes in as revenues, the money that goes out as expenses, the money that is retained as profit, the money that is invested in operational assets, and the money that is owed. It's all about the money. Financial statements follow the money.

The report that measures these daily operations of money in and money out over a period of time is the Income Statement.

Revenues minus Expenses equals Net Income.

The Income Statement can be summarized as Revenues less Expenses equals Net Income. Net Income simply means Income (Revenues) net (less) of Expenses. Net Income is also called Profit or Earnings.

The terms "profits," "earnings" and "net income" all mean the same thing and are used interchangeably. They are synonyms for the bottom line number on the Income Statement. Revenues are often called Sales and are represented on the top line.

You understand the dynamics of this concept intuitively. We always strive to sell things for more than they cost us to make or buy. When you buy a house, you hope it will appreciate in value so you can sell it in the future for more than you paid.

It's also the rule for stocks: buy low, sell high.

The same logic applies to having a sustainable business model in the long run. You can't sell things for less than they cost to make and stay in business for long. So if you own and run a sandwich shop, you had better make sure that you are selling the sandwiches for more than they cost you to make.

Think of the Income Statement in relation to your monthly personal finances. You have your monthly revenues: in most cases the salary from your job. You apply that monthly income to your monthly expenses: rent or mortgage, car loan, food, gas, utilities, clothes, phone, entertainment, etc. Our goal is to have our expenses be less than our income.

There is an old adage: "If you outflow is more than your income, your upkeep is your downfall."

Over time, and with experience, we become better managers of our personal finances and begin to realize that we shouldn't spend more than we make. Instead, we strive to have some money left over at the end of the month that we can set aside and save. In business, what is set aside and saved is called Retained Earnings.

We may invest some of what we set aside with an eye toward future benefits. We may invest in stocks, bonds, mutual funds, or education to expand our future earnings and career prospects. This is the same type of money management discipline that is applied in business. It's just a matter of scale. In business, we buy assets that help the enterprise expand or perform more efficiently. There are a few additional zeros after the numbers on a large company's Income Statement, but the idea is the same.

This concept applies to all businesses. Revenues are usually from Sales of products or services. Expenses are what you spend to support those sales in terms of the operations: Salaries, raw materials, manufacturing processes and equipment, offices and factories, consultants, lawyers, advertising, shipping, utilities etc. What is left over is the Net Income or Profit.

Again: Revenues – Expenses = Net Income.

Net Income is either saved to smooth out future operations and deal with unforeseen events (save for a rainy day); or invested in new facilities, equipment, and technology. Or part of the profits can be paid out to the company owners, called shareholders or stockholders, as a dividend.

The Income Statement is also known as the "profit and loss statement." Business people sometimes use the shorthand term "P&L," which stands for profit and loss statement. A manager is said to have "P&L responsibilities" if they run an autonomous division where they make marketing, sales, staffing, products, expenses, and strategy decisions.

P & L responsibility is one of the most critical responsibilities of any executive position. It involves monitoring the net income after expenses for a department or entire organization, with direct influence on how company resources are allocated and responsibility for performance.

Google the term "income statement," and you will see many examples of formats and presentations. Again, you will see there is variety depending on the industry and nature of the business, but they all follow these basic principles.

Remember: Income (revenue or sales) – Expenses = Net Income or profit

- The Income Statement Guide1:20

Learn Income Statements like a pro! With our guide, discover the basics of financial reporting and boost your financial knowledge!

1️⃣ What is an Income Statement?

An income statement, also known as a profit and loss statement (P&L), is a financial report that shows a company's revenues, expenses, and profits (or losses) over a specific period, typically a fiscal quarter or year.

2️⃣ Components of an Income Statement

Revenue (Sales): The total income from selling goods or providing services.

Cost of Goods Sold (COGS): The direct costs of producing the goods or services.

Gross Profit: Revenue minus COGS, representing the initial profit before operating expenses.

Operating Expenses: Costs related to the day-to-day operations of the business (e.g., salaries, rent, utilities).

Operating Income: Gross profit minus operating expenses, indicating the profit from core operations.

Non-Operating Income (Expenses): Additional income or expenses not directly related to core operations.

Net Income (Profit or Loss): The final result indicates the overall profit or loss after all income and expenses.

3️⃣ Analysis of an Income Statement

To evaluate a company's Income Statement, various margins and ratios are used:

Profit Margin

(Net Income / Revenue) x 100

Gross Margin

(Gross Profit / Revenue) x 100

Operating Margin

(Operating Income / Revenue) x 100

EBITDA Margin:

(EBITDA / Revenue) x 100

Revenue Growth Rate:

((Current Period Revenue – Previous Period Revenue) / Previous Period Revenue) x 100

Return on Equity (ROE):

(Net Income / Shareholders' Equity) x 100

Return on Assets (ROA):

(Net Income / Total Assets) x 100

4️⃣ Interpreting an Income Statement

Positive Net Income: The company is profitable, and the amount represents its earnings for the period.

Negative Net Income: The company incurred losses for the period.

Trends: Analyze trends over multiple periods to assess the company's financial health.

Comparisons: Compare the income statement with those of competitors or industry standards for benchmarking.

5️⃣ Importance of the Income Statement

Investor Insight

Management Tool

Creditworthiness

Strategic Planning

Legal Compliance

Transparency and Trust

Benchmarking

- Quiz for Income Statement: Revenue

- The Income Statement: Expenses11:45

Expenses

Salaries are usually a company's most significant Expense.

Opex vs. Capex.

Opex is short for Operating Expense, and Capex is short for Capital Expense. For example, salaries are an operating expense, and automation or robotics is a capital expense that offsets salaries by reducing the number of employees necessary to run a business.

Capital expenses appear as an asset on the balance sheet and are depreciated in the Income Statement.

COGS cost of goods sold.

Cost of goods sold (COGS) is the direct cost of making a company's products. It is an important line on your income statement that can tell you a lot about your financial performance, efficiency, and profitability.

SG&A

SG&A is an initialism used in accounting to refer to Selling, General, and Administrative Expenses, which is a significant non-production cost presented in an income statement.

Fixed costs

A fixed cost is an expense that a firm incurs that remains the same regardless of how many goods and services are produced or sold. Fixed costs are frequently associated with ongoing expenditures like rent, interest payments, and insurance that are not directly tied to production.

Variable costs

A variable cost is an expense for the firm that varies according to how much is produced or sold. Depending on a company's production or sales volume, variable costs grow or fall. They climb as output rises and reduce as production declines.

A manufacturing company's raw material and packaging costs, credit card transaction fees, or shipping charges, which increase or decrease with sales, are examples of variable costs.

Fixed costs and variable costs can be compared and analyzed.

Break even with revenue.

When determining when you will break even financially, a break-even analysis compares the expenses of a new business, service, or product against the unit sale price. In other words, it indicates when you will have generated enough revenue to pay for all your expenses, both fixed and variable.

Non-cash expenses: AP, depreciation, and amortization

The second most significant Expense in business is usually Taxes.

- 14 Types of Costs You Should Know1:06

14 Types of Costs You Should Know

????? ?? ????????? ?? ???????? ??????

- Relevant/Incremental Costs: Future costs that are relevant to decision-making

- Irrelevant/Sunk Costs: Past costs that are irrelevant to decision-making

????? ?? ????????

- Product Costs: Inventoried costs associated with the production of products or services

- Period Costs: Costs not related to production and expensed in the period

- Manufacturing Costs: total costs associated with the production of goods, including direct materials, direct labor, and manufacturing overhead

- Operating Costs: total costs associated with day-to-day operations

- Conversion Costs: costs incurred when converting raw materials into finished products

- Overhead Costs: indirect costs not tied to a specific product or service, often including items like rent, utilities, and administration costs (can be manufacturing or non-manufacturing)

????? ?? ????????????

- Direct Costs: Costs that can be traced directly to a specific cost object

- Indirect Costs: Costs that cannot be traced directly to a specific cost object

????? ?? ????????

- Fixed Costs: Costs that remain constant regardless of the level of production or services

- Variable Costs: Costs that vary in direct proportion to the level of production

- Semi-variable Costs/Mixed Costs: Costs that contain both fixed and variable components

- Step Costs: Costs that remain fixed only for a certain volume or range of activity

Economic Costs: the total cost of producing your goods or services, including explicit costs (such as wages and materials) and implicit costs (such as opportunity costs).

Allocated Costs: indirect costs that you cannot directly trace to a specific product or service and which you instead distribute to products based on a pre-determined method ideally driven by a cause-effect relationship

- Quiz for Income Statement: Expenses

- The Income Statement: Net Income5:54

Net income. Profit. Earnings

Net income, Earnings, and Profits are synonyms.

In business, as in life, it’s not what you make (revenue). It’s how much you keep (profit). Two ways to achieve more net income: increase revenue or decrease expenses.

EBIT earnings before interest and taxes

EBITDA. Cash flow. Remove distortions of non-cash expenses.

- Quiz for Income Statement: Net Income

- Income Statement Cheat Sheet1:10

Income Statement - Revenue to Net Profit Movement

What causes the change from the revenue to EBITDA to Net Profit?

Observing the movement on the chart below will help you understand the cause of change.

Below are the explanations and calculations for each step depicted on the chart:

Revenue

• Revenue, also known as sales or turnover, is the total amount of money a company generates from its primary business activities.

COGS

• COGS refers to the direct costs associated with producing or manufacturing the goods or services that a company sells.

Gross Profit

• Gross Profit is the amount of money a company has left after subtracting the direct costs of producing its goods or services (COGS) from its total revenue.

• GP = Revenue – GOGS

OPEX

• OPEX are a company’s ongoing costs to operate its business. Include items such as rent, utilities, salaries, and marketing expenses.

Other Income

• Other Income refers to revenue generated by a company that is not directly related to its core business operations. This can include income from investments, interest, or other sources outside the company's primary activities.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

• EBITDA is a measure of a company's operating performance. It excludes interest, taxes, and non-cash expenses like depreciation and amortization.

• EBITDA = GP – OPEX + Other Income

EBIT (Earnings Before Interest & Taxes)

• Depreciation and amortization are non-cash expenses that represent the allocation of the cost of tangible and intangible assets over time.

• EBIT = EBITDA – Depreciation

EBT (Earnings Before Taxes)

• Interest expenses represent the cost of borrowed funds. Subtract interest from the Adjusted EBITDA.

• EBT = EBIT – Interest Expense

Net Profit

• Subtract taxes from Earnings Before Taxes to arrive at Net Profit.

• Net Profit = Earnings Before Taxes - Taxes - Income Statement Synonyms1:04

Income Statements don't have a universal look or layout.

That's because management teams have complete control over the terms & layout of their financial statements.

Here are the other words that management teams can use when creating their Income Statement:

INCOME STATEMENT SYNONYMS:

→Revenue Statement

→Earnings Statement

→Operating Statement

→Statement of Earnings

→Statement of Operations

→Profit and Loss Statement (P&L)

REVENUE SYNONYMS:

→Sales

→Income

→Top Line

→Receipts

→Turnover

→Gross Sales

→Gross Income

COST OF GOODS SOLD SYNONYMS:

→Goods Cost

→Direct Costs

→Cost of Sales

→Cost of Revenue

→Cost of Products Sold

GROSS PROFIT SYNONYMS:

→Sales Profit

→Gross Margin

→Gross Income

→Gross Earnings

OPERATING EXPENSES SYNONYMS:

→Overhead

→Operating Costs

→Operating Outgo

→Sales & Marketing

→Business Expenses

→Operational Expenses

→General & Administrative

→Research & Development

→Selling, General, and Administrative Expenses (SG&A)

OPERATING INCOME SYNONYMS:

→Operating Profit

→Business Income

→Operating Margin

→Operating Earnings

→Operating Cash Flow

→Earnings Before Interest and Taxes (EBIT)

PRE-TAX PROFIT SYNONYMS:

→ Pretax Profit

→ Pretax Earnings

→Income Before Tax

→Profit Before Tax (PBT)

→Earnings Before Tax (EBT)

→Operating Profit Before Tax

→Earnings Before Income Taxes (EBIT)

INCOME TAX SYNONYMS:

→Direct Tax

→Revenue Tax

→Earnings Tax

→Tax on Income

→Corporate Income Tax

→Fiscal Charge on Income

EARNINGS SYNONYMS:

→Profits

→Income

→Earnings

→Net Profit

→Bottom Line

→Net Earnings

→Profit After Tax (PAT)

→Net Income After Taxes

→Earnings After Tax (EAT)

→Net Income Before Extraordinary Items

SHARES OUTSTANDING SYNONYMS:

→Issued Shares

→Outstanding Stock

→Outstanding Equity

→Basic Shares Outsanding

→Diluted Shares Outstanding

→Outstanding Shares of Stock

→Fully Diluted Shares Outstanding

EARNINGS PER SHARE SYNONYMS:

→EPS

→Profit Per Share

→Net Income Per Share

- How to Analyze Profitability0:57

3 Easy Steps to Analyze Business Profitability.

Most business problems fall into one of 3 main areas:

Profitability: How effectively your business generates profit in relation to its expenses.

Cash Flow: The management of the inflow and outflow of cash, ensuring that your business can meet its financial obligations.

Growth: The ability of your business to expand sustainably and profitably.

Financial analysis is a key tool in identifying and addressing these three critical business issues.

Here's how to solve profitability issues:

1️⃣ Gross Profit Margin: (Gross Profit / Revenue) x 100

>> This tells you how efficiently you use raw materials and labor.

>> Drops could be due to increased costs or ineffective pricing.

>> If this margin is dropping, look to renegotiate contracts, trim waste in production, or tweak prices

2️⃣ Operating Profit Margin: (Operating Income / Revenue) x 100

>> This shows how much of each dollar of revenues is left after considering COGS and OPEX (operating expenses).

>> If this margin is dropping, your indirect costs may need to be reviewed because you lack operating flexibility.

3️⃣ Net Profit Margin: (Net Income / Revenue) x 100.

>> Net Profit is what's left of revenues after all expenses and taxes are paid.

>> If this margin is dropping but your other margins are fine, consider tax and debt cost optimization.

>> If this margin drops alongside your other margins, your business model and capital structure may need an overhaul.

- P&L Visualized1:02

The P&L Statement, Visualized

If you're in business, you MUST understand how a Profit & Loss Statement works.

P&L has many different names, including:

Income Statement

Revenue Statement

Earnings Statement

Operating Statement

Statement of Earnings

Statement of Operations

The P&L shows a company's profitability at multiple levels over a period of time using accrual accounting.

Its purpose is to track a company's revenue, expenses, and profits.

Main sections:

? REVENUE: Total Sales

➖ COST OF GOODS SOLD: The cost to deliver the product or service

? GROSS PROFIT: Revenue - Cost of Goods Sold

➖ R&D EXPENSES: All expenses related to developing products & services

➖ SG&A EXPENSES: All other overhead expenses

? OPERATING INCOME: Gross Profit - Operating Expenses

➖ INTEREST EXPENSE: Interest paid to bondholders & banks

? PRE-TAX INCOME: Operating Income - Interest Expense

➖ INCOME TAX: Taxes paid to Governments

? NET INCOME: Pre-Tax Income - Income Tax

To analyze a P&L quickly, focus on changes in margins.

GROSS MARGIN

Gross margin is a profitability metric that indicates the percentage of revenue after subtracting the cost of goods sold (COGS).

Calculation

Gross Margin = Gross Profit / Revenue

Gross Profit = Revenue - COGS

OPERATING MARGIN

Operating margin, or operating profit margin, measures the percentage of operating income (profit after operating expenses) relative to total revenue.

Calculation

Operating Margin = Operating Income / Revenue

NET MARGIN

Net margin, also referred to as net profit margin or simply profit margin, represents the percentage of net income (profit after all expenses, including interest and taxes) relative to total revenue.

Calculation

Net Margin = Net Income / Revenue

- Analyzing the Income Statement1:10

How do we analyze companies?

Start with the income statement.

It can show us the revenues, expenses, and profits over a specific period.

The income statement can give us insights into whether the company is growing or shrinking.

Here is the breakdown of an income statement in its most common form:

???????: This includes all income from sales, services, or other primary business activities.

???? ?? ????? ???? (????): Direct costs attributable to the production of goods sold by a company.

????? ??????: Calculated as Revenue minus Cost of Goods Sold. It represents a company's profit after deducting the costs associated with making and selling its products.

????????? ????????:

???????, ???????, ??? ?????????????? ???????? (??&?): Expenses related to selling products and managing the business.

???????? ??? ??????????? (?&?): Costs of developing new products or services.

????????? ?????? is Earnings Before Interest and Taxes (EBIT), which is calculated by subtracting operating expenses from gross profit.

???????? ???????: The cost incurred by an entity for borrowed funds.

????? ??????/????????: Non-operational revenue or costs, such as gains or losses from investments or foreign exchange.

???-??? ??????: Income before income taxes are deducted.

Income Tax Expense: The amount of tax owed based on pre-tax income.

??? ??????: The final bottom line of the income statement, calculated as Pre-tax Income minus Income Taxes. This figure represents the total earnings attributable to shareholders after deducting all expenses.

Also crucial to analyzing an income statement is margins:

• Gross margin = Gross profit/revenues

• Operating margin = Operating profit/revenues

• Net Income margin = Net Income profit/revenues

Ideally, we want stable or growing margins.

The bottom line is that we want a growing, profitable company that can lead to further digging.

- 4 Types of Income Statement Analysis0:47

4 Types of Income Statement Analysis

1. Vertical Analysis:

Vertical analysis dissects the income statement vertically, showcasing each line item as a percentage of total revenue.

This method offers a snapshot of the proportion of expenses, making it easier to identify trends and assess cost structures.

2. Horizontal Analysis:

By comparing income statements across multiple periods, horizontal analysis unveils the evolution of financial performance over time.

Understanding year-over-year changes aids in identifying growth patterns, potential areas of concern, and overall business stability.

3. Ratio Analysis:

Ratios derived from income statement figures provide a deeper understanding of a company's financial health.

Key ratios like the profit margin, return on assets, and earnings per share offer valuable insights into profitability, efficiency, and overall operational effectiveness.

4. Common Size Analysis:

This analysis involves expressing each line item as a percentage of total revenue.

It provides a standardized view of the income statement, facilitating comparisons across different companies or industries.

Common size analysis helps investors and analysts evaluate the relative importance of each expense category.

Embracing these diverse analytical approaches empowers financial professionals to make informed decisions, assess risk, and strategize for sustained business success.

- The Balance Sheet15:10

Balance Sheet Basics

The Balance Sheet is a condensed statement that shows the financial position of an entity on a specified date, usually the last day of an accounting period.

Among other items of information, a balance sheet states

What Assets does the entity own,

How it paid for them,

What it owes (its Liabilities), and

What is the amount left after satisfying the liabilities (its Equity)

Balance sheet data is based on what is known as the

Accounting Equation: Assets = Liabilities + Owners' Equity.

Think of a Balance Sheet in terms related to everyday life. For example, homeownership, when you have a mortgage, is represented as a Balance sheet. Your home ownership has the three components of Asset, Liability, and Equity.

The Asset is the value of the house. An appraisal determines this. An appraisal considers recent sales of homes in the area and compensates for differences like the number of bath or bedrooms, the size of the lot, etc.

The Liability is the mortgage. This debt is how much you owe against the house.

Equity is the difference between the asset's value and the Liability amount. For example, if your home is worth $200,000 and you have a remaining mortgage balance of $150,000, then you have $50,000 in Equity. We sometimes call this homeowner's Equity.

If your mortgage balance is more than the value of the home, then you are considered "upside down" or "underwater." The same principle applies to a business: if the value of its Liabilities is more than the value of the Assets, then the enterprise is insolvent and probably headed for bankruptcy.

A Balance Sheet is organized under subheadings such as current assets, fixed assets, current liabilities, Long-term Liabilities, and Equity.

The Balance Sheet, along with the income and cash flow statements, comprises the financial statements, a set of documents indispensable for running a business.

What does the Balance Sheet balance?

The balance sheet is structured to show the amount and type of assets an enterprise owns and how those assets are funded. One side of the balance sheet shows what you have (assets), and the other side shows how you paid for it (Debt and Equity).

Assets can be purchased and paid for in two ways: with debt or with Equity (or a combination of the two). What a company owes, the obligations or loans, are called Liabilities; what a company owns is the Equity or Stock.

The Liabilities and Equity are equal to the Assets. Therefore, they are two sides of the same coin and must balance, hence the term Balance Sheet.

This balancing is a fundamental principle of Accounting called the Accounting Equation. Assets = Liabilities + Equity.

Balance Sheet Format

A Balance Sheet is typically organized in two columns, with the Assets on the left and the Liabilities and Equity on the right. It is divided into subcategories, with the most current types on top and the more long-term varieties towards the bottom.

Current Assets are ones like cash that can be used on short notice, and Long term Assets are things like factories that would take longer to convert to cash—current means short-term, stuff that needs to be addressed within one year. Long-term means stuff longer than the next year.

Bills that need to be paid within the month are considered Current Liabilities, and loans that are paid back over years are regarded as Long term Liabilities.

Equity is what the owners actually own. Equity is basically Assets less Liabilities and is shown as accounts below the Liabilities on the left-hand side. Equity is shown below the Liabilities because debt has senior claims on the assets.

In the event of liquidation like bankruptcy, the debt holders get paid from the sale of assets first, and then anything left over goes to the equity holders.

Here is an example Balance Sheet to get and idea of the format; notice that the Total Assets equals the Total Liabilities plus Equity.

- Balance Sheet Graphically Explained0:40

The Balance Sheet Explained Simply

The master equation: Assets = Liabilities + Shareholder Equity

TIME: The Balance Sheet records a Point in Time

ACCOUNTING METHOD: Accrual

3 Main Sections:

ASSETS: What the company Owns

LIABILITIES: What the company Owes to creditors

EQUITY: The net value of the owner's claim

ASSETS

They are listed in order of liquidity (how quickly it can be turned into cash).

CURRENT ASSETS: Expected to be used in <1 year

→Cash

→Marketable Securities

→Accounts Receivable

→Inventory

→Other Current Assets

LONG-TERM ASSETS: Expected to be last >1 year

→Long-Term Investments

→Fixed Assets

→Goodwill

→Other Long-Term Assets

LIABILITIES

Listed in order of when they are expected to be paid off.

CURRENT LIABILITIES: Expected to be paid in <1 year

→Payables & Accrued Expenses

→Short-Term Debt

→Other Current Liabilities

LONG-TERM LIABILITIES: Expected to be paid in >1 year

→Long-Term Debt

→Other Long-Term Liabilities

SHAREHOLDER'S EQUITY

CAPITAL RAISED FROM INVESTORS

→Preferred Stock

→Common Stock & Additional Paid-In Capital

PROFITS RETAINED BY THE COMPANY

→Retained Earnings

→Treasury Stock

- How to Read a Balance Sheet0:18

I'll teach you How to Read a Balance Sheet in 7 minutes.

I've spent 30+ years studying Finance, with 15 as a public company CFO.

This post is a "cheat sheet" ebook on how to read a Balance Sheet in 7 minutes:

• What does the balance sheet tell you?

• What is the structure of the balance sheet?

• What are Assets?

• What are Liabilities?

• What is Equity?

• How do you analyze a balance sheet?

- How to Analyze a Balance Sheet0:48

Here is a quick analysis of the balance sheet:

??????? ??????

Calculate the working capital (current assets - current liabilities) to assess the company's liquidity.

????

calculate cash to short-term liabilities to review any potential liquidity issues in the very short term.

??????? ???????????

Calculate dso to see how quickly the company collects cash.

???????????

Calculate dio to see how the company is efficient in converting inventories into cash

????? ??????

Check the efficiency with fixed asset turnover evaluation.

Evaluate fair value, especially for intangibles.

??????? ???????????

Calculate the current ratio and quick ratio to assess liquidity.

??????? ????????

Calculate Days Payable Outstanding (DPO) to track how quickly a company pays a bill and tends to prolong terms.

????? ???? ????

The top priority in payment. Make sure the company is able to meet its immediate financial obligations.

???-??????? ????

Evaluate debt-to-asset ratio to determine solvency.

??????

Calculate the equity ratio (equity / total assets) to understand stability

ROE (net income/equity) to understand the profitability

???? ???? ??? ?? ???? ?? ????? ????????

1. understand the meaning of the ratio

2. result interpretation

3. compare with last period, budget and industry peers

4. action plan

- Balance Sheet Analysis0:49

Here's how you can be a financial expert by analyzing balance sheets:

?????????? ??? ??????:

==============

Grasp the fundamental concepts of assets, liabilities, and equity. Familiarize yourself with the balance sheet equation: Assets = Liabilities + Equity.

??????? ??????? ??? ???-??????? ??????:

==========================

Assess the company's ability to convert its assets into cash within a year. Evaluate the value of long-term assets like property, plant, and equipment.

?????????? ???????????:

============

Evaluate the company's short-term and long-term obligations. Understand how these obligations impact the company's financial flexibility.

??????? ?????? ???????????:

==================

Analyze the company's common stock and retained earnings. Assess the ownership structure and the company's ability to generate profits over time.

?????? ??? ??????:

============

Utilize ratios like the current ratio, debt-to-equity ratio, and debt-to-asset ratio to gain insights into the company's financial strength and efficiency.

???????? ????????? ???? ?????:

=================

Be vigilant about red flags like increasing accounts receivable, rising inventory, and high debt levels. These signals could indicate potential financial risks.

????????? ??? ???????:

================

Benchmark the company's balance sheet ratios against industry peers to assess its relative financial position.

??????? ?????????? ????????:

====================

Financial analysis is not an exact science. To enhance your expertise, stay informed about financial trends, accounting standards, and industry developments.

- Depreciation0:46

DEPRECIATION

DEPRECIATION is an accounting method used to allocate the cost of tangible assets (such as buildings, machinery, and vehicles) over their useful lives. It represents the systematic reduction in an asset's value due to wear and tear, obsolescence, or other factors.

Depreciation happens to TANGIBLE Assets (you CAN touch them)

Examples:

Car

Equipment

Buildings

3 DEPRECIATION METHODS

STRAIGHT - LINE

The most common and easiest method to calculate depreciation. To use this depreciation method, you need to divide the cost of an asset by the useful life of an asset (in years).

FORMULA: Cost / Useful Life

DECLINING BALANCE

Used to calculate large depreciation expenses or assets that quickly lose value. Multiply the opening book value by the depreciation rate.

FORMULA: Opening book value x (100% / Useful Life of asset)

SUM OF THE YEARS DIGITS

An accelerated depreciation method increases the expense in the early years and lowers it in the latter years. Multiply the cost of an asset by its useful life over the sum of the years digits.

FORMULA: Cost x ( Useful life / Sum of the Years digits)

See the infographic for examples!

- Quiz on the Balance Sheet

- The Cash Flow Statement10:05

The cash flow statement is a financial document that provides detailed data regarding all cash inflows a company receives from its ongoing operations and external investment sources and all cash outflows that pay for business activities and investments during a given period. It is one of the three fundamental financial statements used to assess a company's performance and financial health; the other two are the income statement and the balance sheet.Here are the key components of a cash flow statement:

Operating Activities: This section shows the cash flow from day-to-day business operations. It starts with net income and then reconciles all non-cash items to cash items involving operational activities. This includes adjustments for depreciation, changes in accounts receivable and payable, and changes in inventory.

Investing Activities: This section reports cash flow from all investing activities. It includes purchases of physical assets, investments in securities, or the sale of securities or assets. Negative cash flow here could indicate that the company is investing in its future growth.

Financing Activities: This section reflects the cash flow from financing activities like issuing stock, paying dividends, and borrowing. It explains how a company finances its operations and growth through debt, equity, and dividend policies.

Net Increase or Decrease in Cash: This section shows the net change in the company's cash position over the period. If the closing balance of cash and cash equivalents is higher than the opening balance, the company has a net increase in cash.

Beginning and Ending Cash Balance: The statement starts with the amount of cash on hand at the beginning of the period and ends with the amount of cash at the end of the period.

The cash flow statement is essential for understanding a company's liquidity, solvency, and overall financial health. It shows how well a company manages its cash position, indicating whether it can generate enough cash to meet its debt obligations and fund its operating expenses. Unlike the income statement, it's immune to accounting assumptions and is a good indicator of a company's financial strength and ability to generate cash to fund operations.

- EBITDA explained0:45

EBITDA Explained

What is EBITDA, and what is your take on this metric?

EBITDA stands for:

• Earnings

• Before:

• Interest

• Taxes

• Depreciation

• Amortization

It's a financial metric that shows how much money a company makes before accounting for non-operational expenses like interest and taxes and non-cash expenses like Depreciation and Amortization.

Why is EBITDA important for Businesses?

EBITDA is important because it gives businesses an idea of how much money they generate from their operations.

This is useful for investors and lenders who want to know how profitable a company is.

It's like a scorecard to know how much money a company is making.

How is EBITDA calculated?

To calculate EBITDA, start with a company's revenue and subtract its cost of goods sold.

Then, you subtract its operating expenses (like salaries and rent).

Another way to calculate it:

Net Income

+ Interest Expense

+ Taxes

+ Depreciation

+ Amortization

EBITDA vs. Net Income

EBITDA:

In EBITDA, you don't consider these expenses: Depreciation, Taxes, and Interest.

Net Income:

However, net income is what remains as actual profit after Depreciation, interest, and taxes are taken into account.

- Cash Flow Statement Terminology1:20

Cash Flow Statements do not have a universal look or layout.

That's because management teams control the terms and categories of their financial statements.

Here are the other words that management teams can use when creating their Cash Flow Statement:

CASH FLOW STATEMENT SYNONYMS:

→Cash Statement

→Statement of Cash Flow

→Financial Flow Statement

→Statement of Financial Flows

→Statement of Cash Operations

NET INCOME SYNONYMS:

→Profits

→Income

→Earnings

→Profit After Tax

→Earnings After Tax

NON-CASH CHARGES

→Depreciation

→Amortization

→Write-downs

→Deferred Taxes

→Impairment Charges

→Stock-based Compensation

→Unrealized Gains and Losses

CHANGES IN WORKING CAPITAL

→Credits

→Accruals

→Payables

→Provisions

→Inventories

→Receivables

→Prepayments

OPERATING CASH FLOW

→Cash Profit

→Cash Income

→Operating Cash

→Cash from Operations

→Cash Generated from Operations

→Net Cash from Operating Activities

CAPITAL EXPENDITURES:

→Capex

→PPE Spend

→Plant Outlay

→Property Spend

→Facilities Spend

→Equipment Spend

→Infrastructure Spend

→Property, Plant, and Equipment

ACQUISITIONS:

→Merger

→Takeover

→Asset Buy

→Consolidation

→Company Purchase

→Corporate Acquisition

PROCEEDS FROM SALE OF INVESTMENTS

→Sale Gain

→Disposal

→Asset Sale

→Divestiture

→Liquidation

→Sale Proceeds

→Disposal of Investments

→Proceeds from Sales of Assets